Accounting ACCT 2610 Chapter Notes - Chapter 6: Gross Margin, Direct Deposit, Promissory Note

22 Feb 2017

School

Department

Course

Professor

• gross profit (gross margin, gross profit margin) = net sales revenue – cost of

sales

• revenue principle requires that revenues be recorded when they are earned

(delivery has occurred or services have been rendered, there is persuasive

evidence of an arrangement for customer payment, the price is fixed or

determinable, and collection is reasonably assured)

o for sellers of goods, these criteria are most often met and sales revenue is

recorded when title and risks of ownership transfer to the buyer

▪ the point at which title (ownership) changes hands is determined

by the shipping terms in the sales contract

• when goods are shipped FOB (free on board) shipping

point, title changes hands at shipment, and the buyer

normally pays for shipping

o revenues are normally recognized at shipment

o most companies recognize revenue at shipment

• when goods are shipped FOB destination, title changes

hands on delivery, and the seller normally pays for shipping

o revenues are usually recognized at delivery

o service companies most often record sales revenue when they have

provided services to the buyer

• the appropriate amount of revenue to record is the cash equivalent sales price

• companies use different methods to motivate customers to buy products and

pay for their purchases

▪ all these affect net sales revenue computing

o allowed to use credit cards to pay for purchases

o provide business customers direct credit and discounts for early payment

o allowing returns from all customers under certain circumstances

• credit card sales to consumers

o credit card discount = the fee charged by the credit card company for

services, a contra-revenue

▪ credit sales revenue ()

• credit card discounts () = total credit card sales x credit

card discount

▪ sales revenue – credit card discounts = net sales (reported on the

income statement)

• sales discounts to businesses

o some sales to businesses are credit sales on open account; there is no

formal written promissory note or credit card

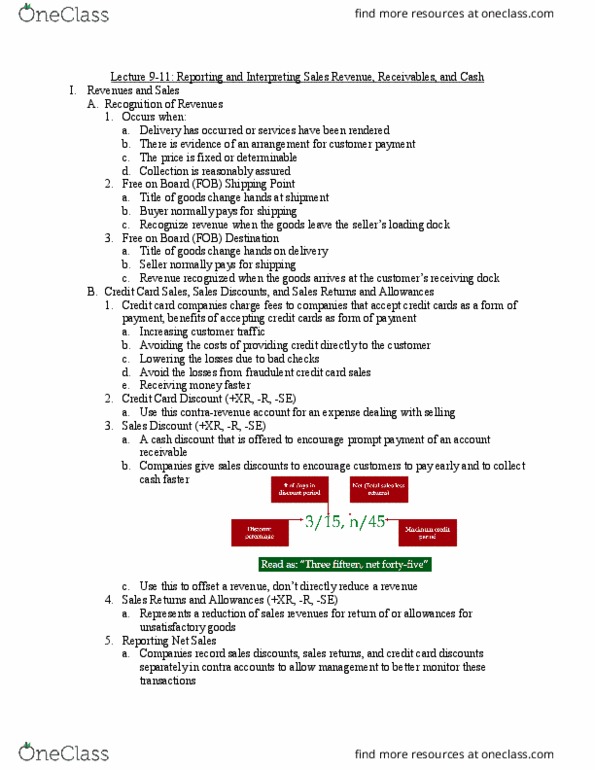

o credit terms printed on invoice as an early payment incentive

▪ early payment incentive

• 2/10,n/30

• 2 = discount percentage

• 10 = number of days in discount period

• n = net (total sales – returns)

• 30 = maximum credit period

find more resources at oneclass.com

find more resources at oneclass.com

o sales discount (cash discount) = a cash discount offered to encourage

prompt payment of an account receivable, a contra revenue → credit

terms

▪ credit sales revenue ()

• sales discounts () = discount percentage x sales

▪ sales revenue – sales discounts = net sales

o if payment is made after the discount period, the sales discount doesn’t

apply

• sales returns and allowances

o sales returns and allowances = a reduction of sales revenue for return

of or allowances for unsatisfactory goods, a contra-revenue

▪ credit sales revenue ()

• sales returns and allowances () = (goods returned/total #

of goods purchased) x sales

• reporting net sales

o reported on the income statement

▪ credit sales revenue (R)

• - debit credit card discounts (XR)

• - debit sales discounts ( XR)

• - debit sales returns and allowances (XR)

▪ = net sales (reported on the income statement)

• gross profit percentage = measures a company’s ability to charge premium

prices and produce goods and services at low cost

o a higher gross profit results in higher net income

o gross profit/net sales

• classifying receivables

o account receivable (trade receivables, receivables) = open accounts

owed to the business by trade customers

▪ created by a credit sale on an open account

o note receivable = written promises that require another party to pay the

business under specific conditions (amount, time, interest)

▪ promise in writing to pay a specified amount of money, the

principal, and a specified amount of interest at a future date

o receivables may be classified as trade or nontrade recievables

▪ trade receivable = created in the normal course of business when

a sale of merchandise or services on credit occurs

▪ nontrade receivable = created from transactions other than the

normal sale of merchandise or services

o in a classified balance sheet, receivables are classified as current (short-

term) or non-current (long-term) depending on when the cash is

expected to be collected

• accounting for bad debts

o when a company extends credit to noncommercial customers, it knows

that some of these customers will not pay their debts

find more resources at oneclass.com

find more resources at oneclass.com