ACCT 2331 Chapter Notes - Chapter 8: Current Liability, Contingent Liability, Financial Statement

31 Mar 2017

School

Department

Course

Professor

Document Summary

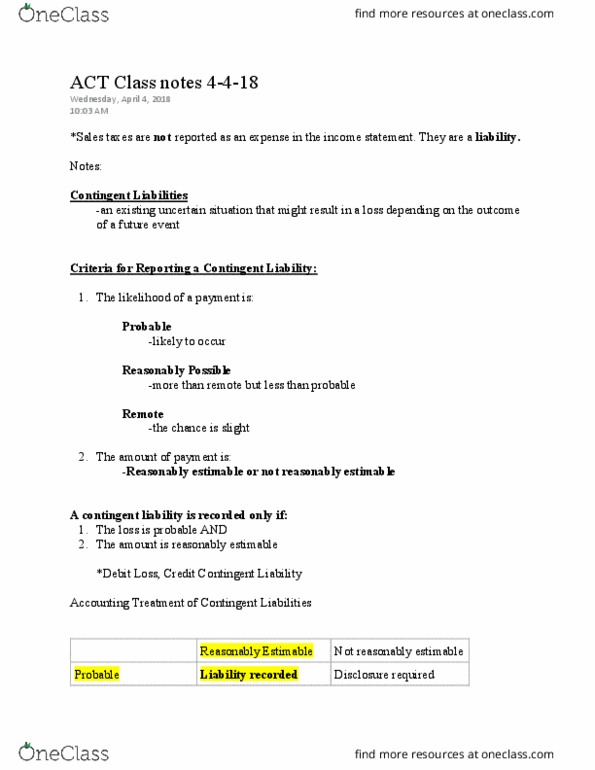

Taxes collected for taxing authorities are recognized as current liabilities. The current portion of long-term debt, is the amount that will be paid within the next year. Criteria used to determine whether a contingent liability is reported in the financial statements: likelihood of loss. Probable: likely to occur: the ability to estimate the amount of the loss. Contingent liability: an existing uncertain situation that might result in a loss depending on the outcome of a future event: frequent flier program awards, future litigation losses, product warranties. The flipside of a contingent gain is a contingent loss. A loss that judged to be probable and for which the amount is reasonably estimable should be accrued. Nash"s attorney estimates the company must pay ,000 - ,000 relating to the current litigations, and the loss will most likely be equal to ,000. Nash should accrue a contingent liability and loss of ,000.