ECON 1 Chapter Notes - Chapter 5: Average Variable Cost, Marginal Revenue, Marginal Cost

85

ECON 1 Full Course Notes

Verified Note

85 documents

Document Summary

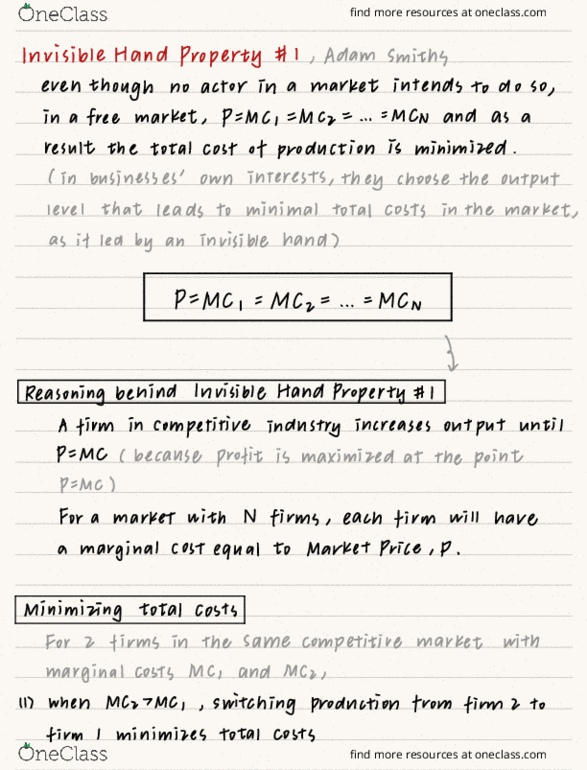

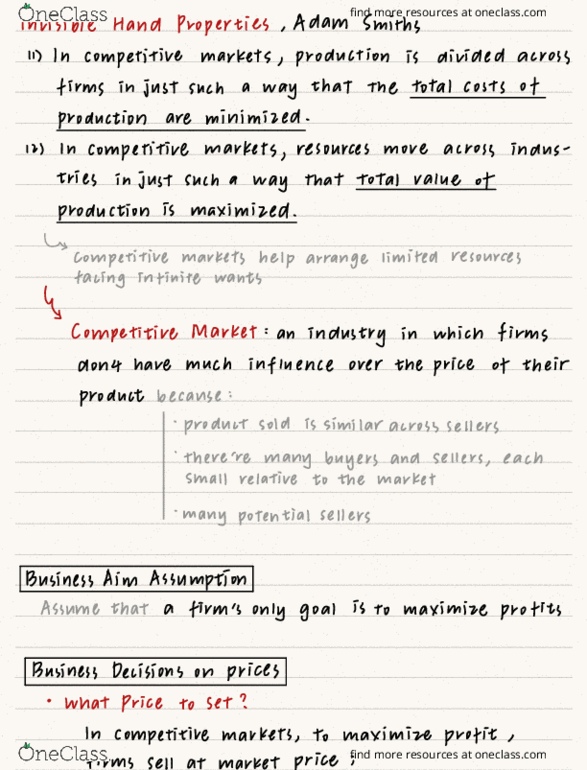

In a competitive market, production is divided across firms in just such a way that total costs of production are minimized. Resources move across industries in just such a way that total value of production is maximized. In perfect competitive industry, firms don"t have much influence over the price of their product under the following conditions: The product being sold is similar across sellers. There are many buyers and sellers, each small relative to the total market. Total revenue is the price times quantity sold: tr = p * q. Total cost is the cost of producing a given quantity of output. Fixed costs are costs that do not vary with output. Variable costs are costs that do vary with output. Marginal revenue mr is the change in total revenue from selling an additional unit. For a firm in a competitive industry, mr = price. Marginal cost mc is the change in total cost from producing an additional unit.