ECON 1 Chapter Notes - Chapter 5: Time Horizon, Midpoint Method, Normal Good

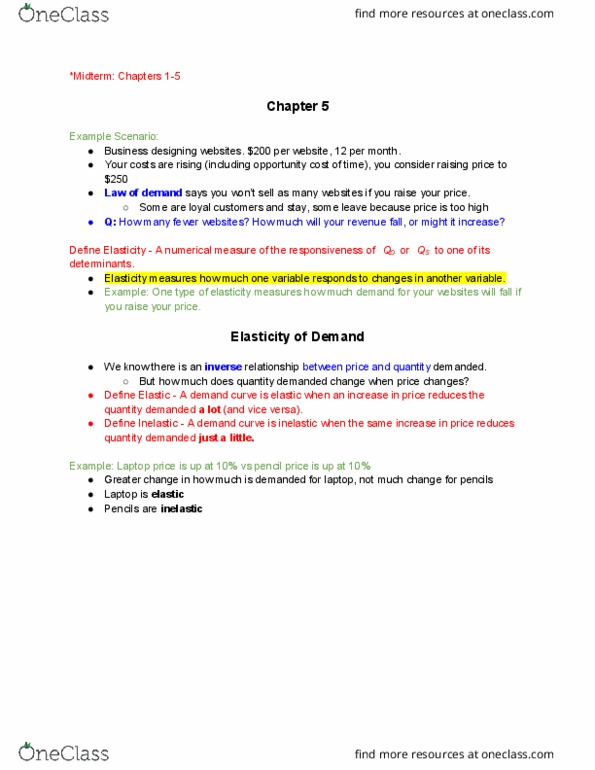

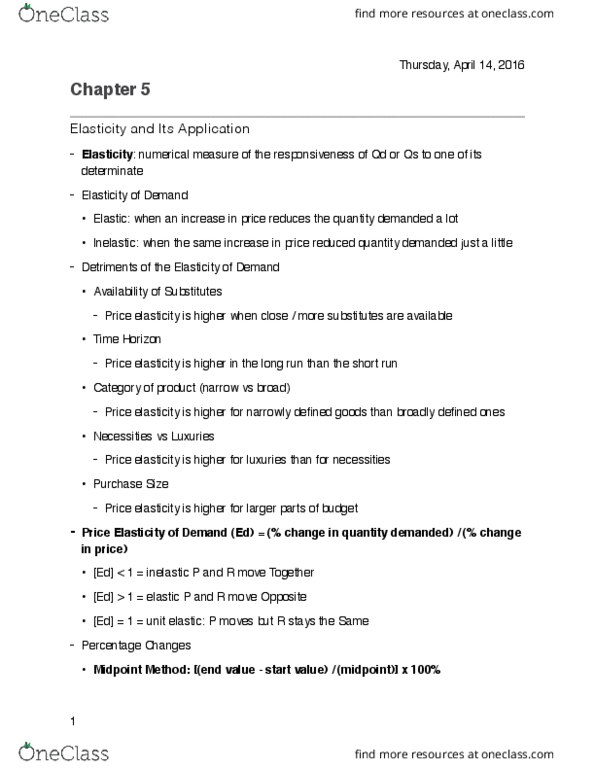

Chapter 5

Elasticity is a measure of how much buyers and sellers respond to changes in market

conditions.

Elasticity of demand

Consumers buy more of a good when the price is lower, when their income is higher, when the

prices of the substitutes are higher or when the prices of its complements are lower. We

discussed demand in quality not quantity. Elasticity measures how much consumers respond to

changes in price and quantity demanded.

The law of demand states that a fall in the price raises the quantity demanded, the price

elasticity of demand measures how much the quantity demanded responds to a change in

price.

Demand for a good is said to be elastic if the quantity demanded responds to changes in the

price a lot; inelastic if the response is small.

There are some rules of thumb about what influences the price elasticity:

1) Availability of close substitutes

If there are no close substitutes, the increase in price won’t really affect the quantity demanded.

(inelastic)

2) Necessities vs Luxuries

Necessities tend to have inelastic demands, whereas luxuries have elastic demands.

3) Definition of the market

The elasticity of demand in any moarket depends on how we draw the boundries of the market:

if the market is narrowly defines, the market tends to have more elasticity than broadly defined

markets because it’s easier to find close substitutes for narrowly defined good. (i.e finding a

substitute for food vs apple)

4) Time horizon

Goods tend to have more elastic demand over longer time horizons.

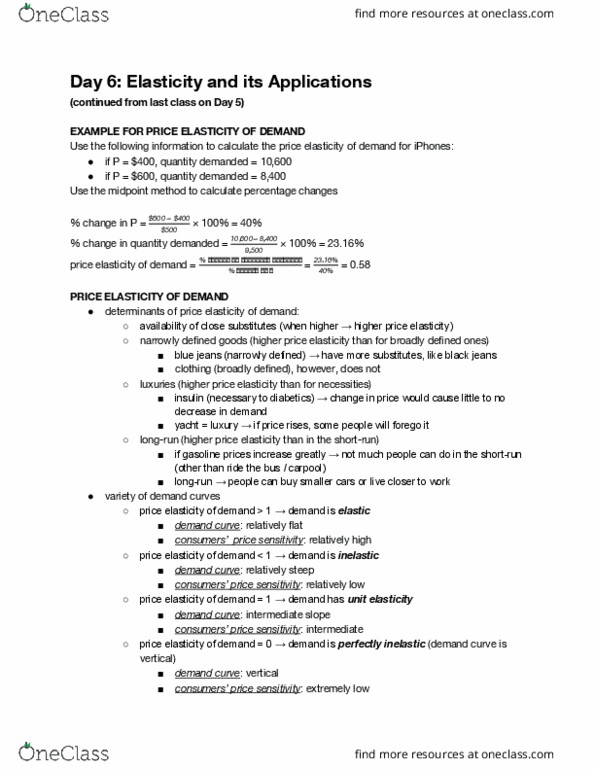

Computing the price of elasticity of demand:

Price elasticity of demand = Percentage change in quantity demanded / percentage change in

price

**because the quantity demanded of a good is negatively related to its price, the percentage

change in quantity will always have the opposite sign as the percentage change in price. Here

we drop the minus sign and report the absolute value. So a larger prices elasticity implies a

greater responsiveness of quantity demanded.

The midpoint method:

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Elasticity is a measure of how much buyers and sellers respond to changes in market conditions. Consumers buy more of a good when the price is lower, when their income is higher, when the prices of the substitutes are higher or when the prices of its complements are lower. Elasticity measures how much consumers respond to changes in price and quantity demanded. The law of demand states that a fall in the price raises the quantity demanded, the price elasticity of demand measures how much the quantity demanded responds to a change in price. Demand for a good is said to be elastic if the quantity demanded responds to changes in the price a lot; inelastic if the response is small. There are some rules of thumb about what influences the price elasticity: availability of close substitutes. If there are no close substitutes, the increase in price won"t really affect the quantity demanded. (inelastic: necessities vs luxuries.