ACCT 2301 Chapter Notes - Chapter 7: Gross Margin, Interest Expense, Income Statement

22 Mar 2016

School

Department

Course

Professor

Document Summary

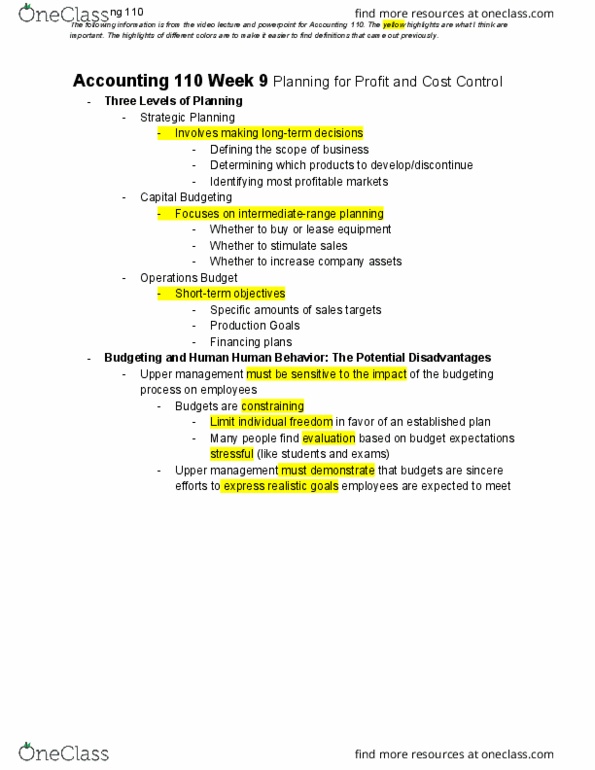

Short term planning focuses on the coming year which are specific and detailed. Strategic planning: involves making long term decisions such as defining the scope of the business, determining which products to develop or discontinue, and identifying the most profitable market niche: descriptive rather than quantitative. Capital budgeting: focuses on intermediate range planning: whether to buy or lease equipment, whether to stimulate sales or increase asset base. Operating budgeting concentrates on short term plans: master budget: describes short term objectives in specific amounts of sales targets, production goals, and financing plans. Planning: the budget formalizes and documents managerial plans, clearly communicating objectives to both superiors and subordinates. Performance measurement: budgets are specific, quantitative representations of management"s objectives. Corrective action: budgeting provides advance notice of potential shortages, bottlenecks, or other weaknesses in operating plans. Upper level managers must demonstrate that they view the budget as a sincere effort to express realistic goals employees are expected to meet.