ACCT 2101 Chapter Notes - Chapter 2: Cost Driver, Indirect Costs, Expense

Document Summary

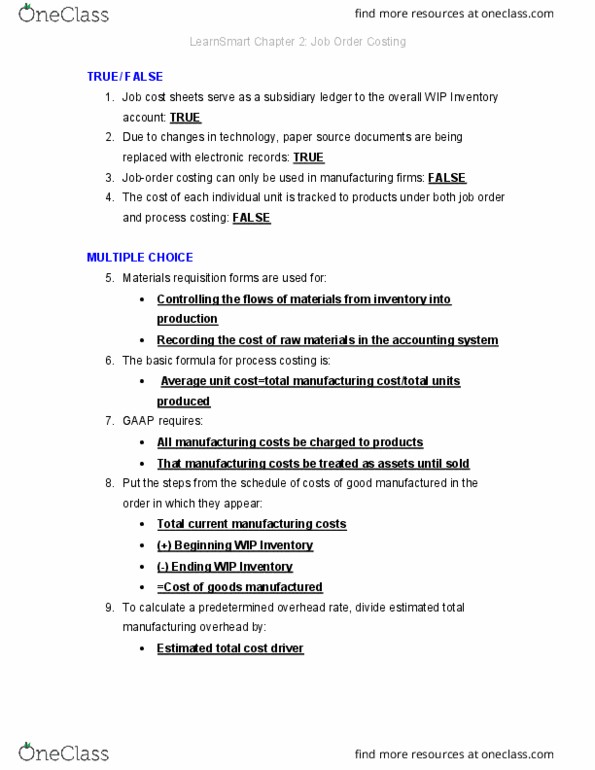

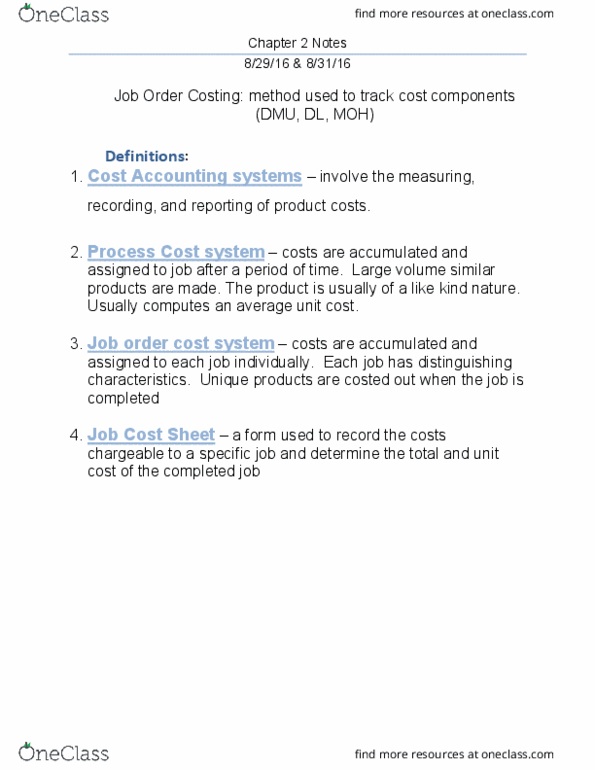

Acct 2101: chapter 2 summary: describe how costs flow through the accounting system in job order costing. Initially, raw materials purchases are recorded in the raw. Materials inventory account: when materials are placed into production, direct materials are recorded in the work in process inventory account; indirect materials are recorded in the manufacturing. Overhead account: when labor costs are incurred, direct labor is recorded in the work in process inventory account; indirect labor is recorded in the. Manufacturing overhead account: when manufacturing overhead is applied to specific jobs, the work in process inventory account is debited and the manufacturing. Overhead account is credited: when a job is completed, the total cost of goods completed is transferred from the work in process inventory account to the. Finished goods inventory account: when the job is delivered to the customer, the total cost is transferred from finished goods inventory to the cost of goods.