BUS-A 202 Chapter Notes - Chapter 3: Contribution Margin, Activity-Based Costing, Earnings Before Interest And Taxes

Document Summary

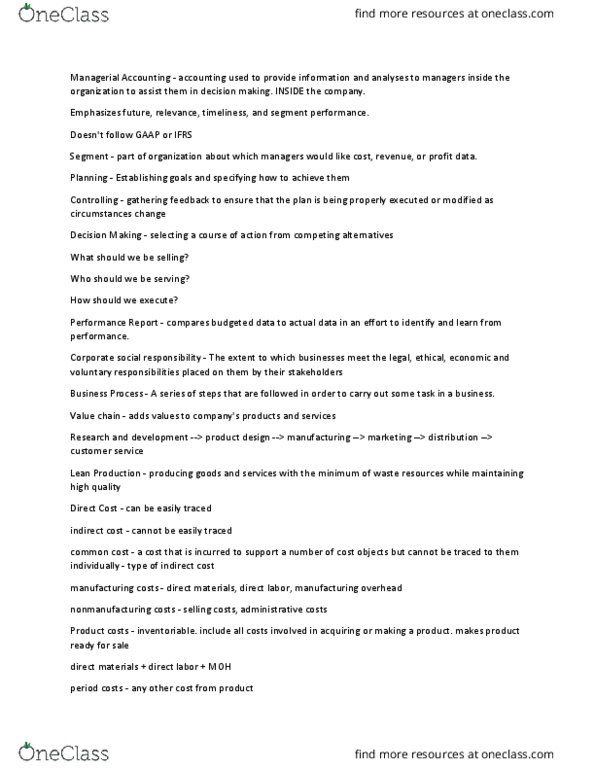

Inventoriable costing absorption costing - dm + dl + vmoh + fmoh. Inventoriable costing variable costing - dm + dl + vmoh. Unit contribution margin - cm/units step cost - a cost function that is fixed over a range, and then increases by a measured step to a new level at the next higher increment of activity. High-low method variable costs - high cost - low cost / high activity - low activity. Breakeven units - (fc + target profit) cm/unit in sales dollars. Breakeven revenue - breakeven unit * selling price. Variable cost % - 1 - cm ratio. Target units - (fc + target) cm/unit. Target revenue - (fc + target) / contribution margin ratio. Margin of safety - actual (or budgeted) sales - breakeven sales. Margin of safety percentage - (actual (or budgeted) sales - breakeven sales) actual (or budgeted) sales.