BUS 215 Chapter Notes - Chapter 5: Operating Leverage, Earnings Before Interest And Taxes, Contribution Margin

Document Summary

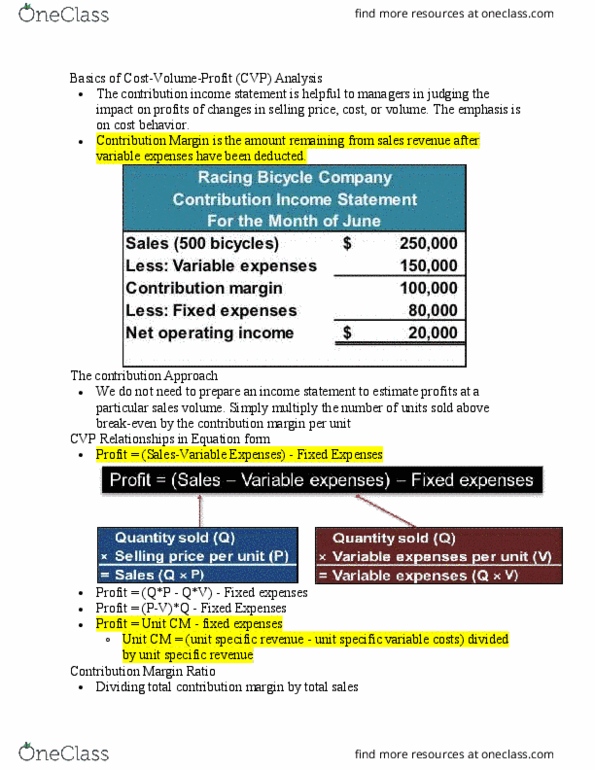

Costs are linear and can be accurately divided into variable and fixed. In multiproduct companies, the mix of products sold remains constant components. Lo 1: explain how changes in activity affect contribution margin and net operating income have been deducted. Contribution margin is the amount remaining from sales rev after variable expenses. Remaining is used to cover fixed expenses and the leftover is profits/losses. By selling one more unit, net income/loss increases/decreases by the unit sale price. The break-even point occurs when contribution margin = fixed expenses, so net. Increase in net income = # additional units above cm sold x cm/unit sale price. If single product operating income = sh. Lo 2: prepare and interpret a cost-volume-profit (cvp) graph and a profit graph. The relationships among revenue, cost, profit, and volume are illustrated in a cost- volume profit (cvp) graph(break-even chart) Highlights relationships over wide ranges of activity.