ACC 202 Chapter Notes - Chapter 4: Finished Good, Financial Statement, Weighted Arithmetic Mean

Document Summary

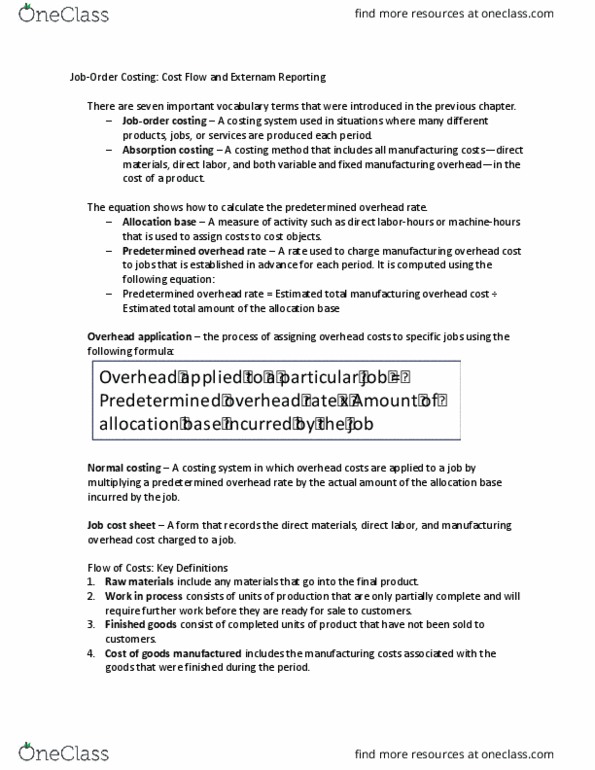

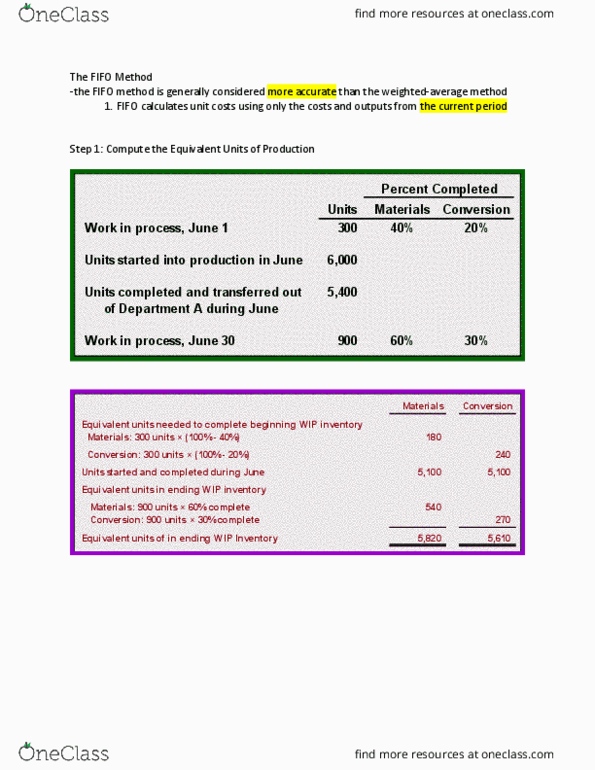

Both systems assign material, labor, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use the same manufacturing accounts, including manufacturing. Overhead, raw materials, work in process, and finished goods. The flow of costs through the manufacturing accounts is basically the same in both systems. Any unit in an organization where materials, labor, or overhead are added to the product. The activities performed in a processing department are performed uniformly on all units of production. Furthermore, the output of a processing department must be homogeneous. Products in a process costing environment typically flow in a sequence from one department to another. Direct materials, direct labor, and moh costs are traced and applied to departments in a process cost system (as opposed to jobs in a job order costing system) The key to deriving these two numbers is calculating unit costs within each department.