ADMS 4551 Chapter Notes - Chapter 3: Legal Liability, Professional Ethics, Professional Code Of Quebec

4 Nov 2018

School

Department

Course

Professor

Document Summary

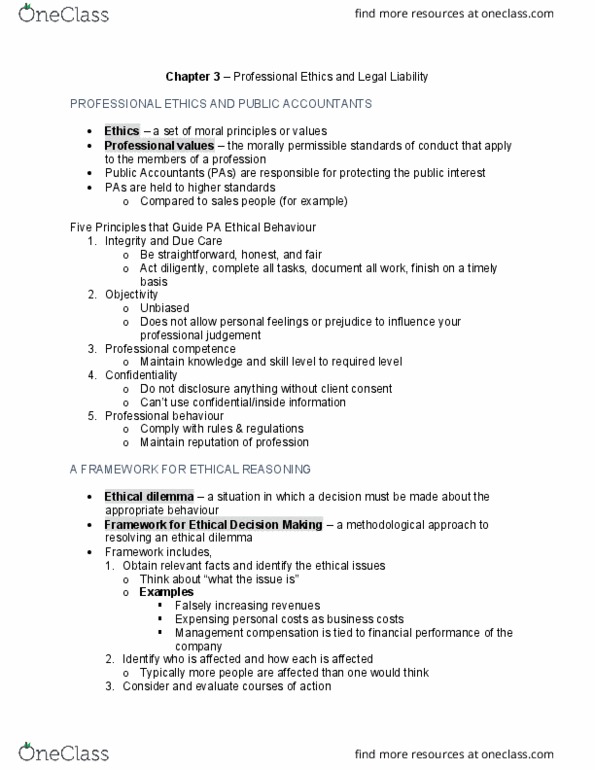

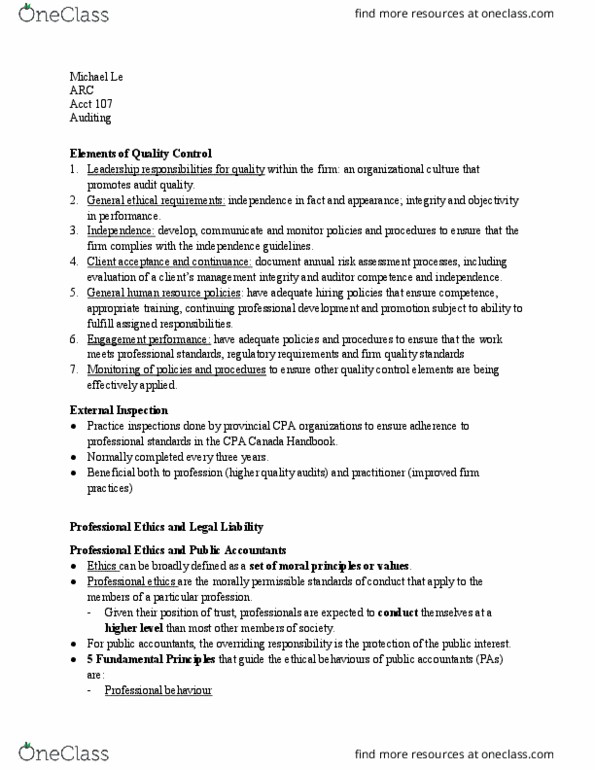

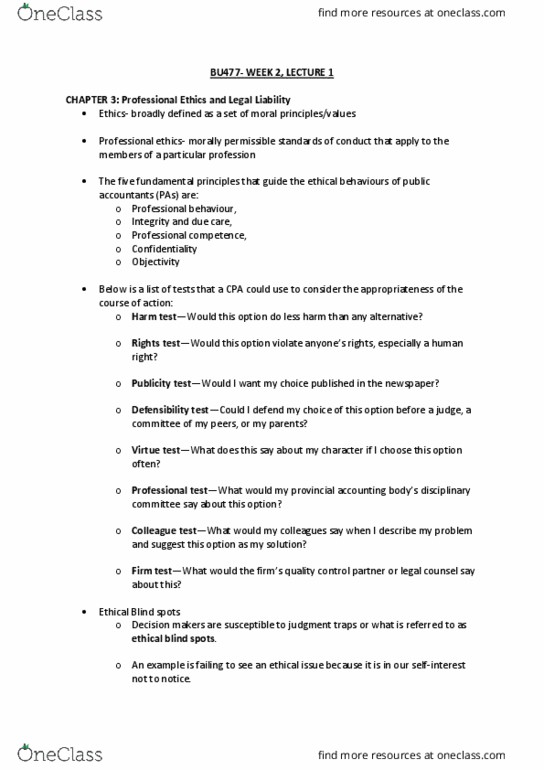

Identify who is affected & how: bryan / martha / karen / staff in future may not meet budget / other staff in firm. Look long term & short term: potential rationalizations, avoid unethical behavior, test course of action, tests, harm / rights / publicity/ defensibility/virtue/professional/colleague / firm. Integrity hallmark of profession: a(cid:272)(cid:272)ou(cid:374)ta(cid:374)t"s asset honesty & fair dealing. Independence in fact auditor maintain unbiased attitude throughout audit. Independence in appearance users believe them to be advocates. If subpoenaed by court does not require permission by client. Lose relationship if disclose info: but client can challenge court, rule 210 conflicts of interest. If provide assurance for 2 competitors: rule 211 duty to report breaches of cpa code. If colleague breaches rule report to discipline committee. Independence standard for assurance engagement: rules 204-204. 10 provide framework assess independence. If implemented system but later find out faulty: familiarity threat personal relationships with client threaten objectivity.