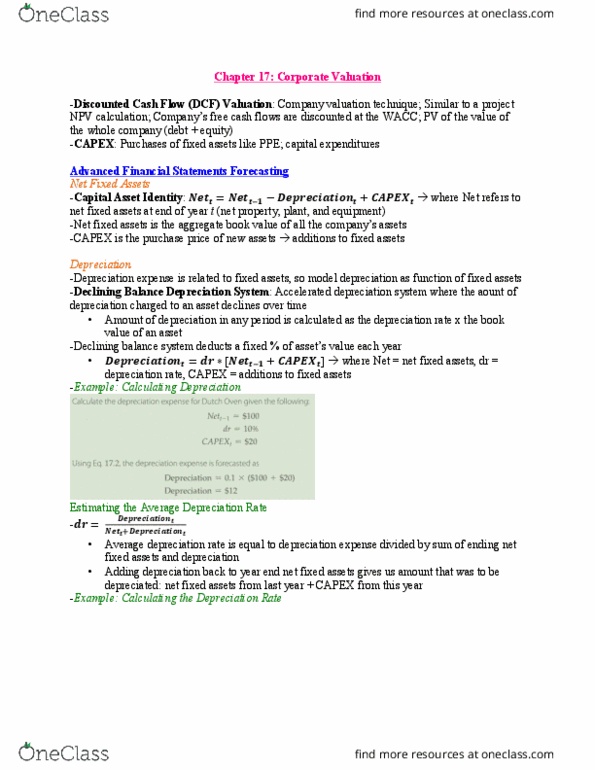

BU393 Chapter Notes - Chapter 10: Capital Cost Allowance, Capital Budgeting, Tax Shield

Document Summary

Chapter 10: capital budgeting - estimating cash flows. Based o(cid:374) a de(cid:272)li(cid:374)i(cid:374)g (cid:271)ala(cid:374)(cid:272)e dep(cid:396)e(cid:272)iatio(cid:374) (cid:373)ethod a(cid:374)d assig(cid:374)s assets to (cid:858)p(cid:396)ope(cid:396)t(cid:455) (cid:272)lasses(cid:859) Each property class has a different depreciation rate. Ucc(t-1) = the undepreciated capital cost at the end of the prev year (year t-1) The (cid:272)apital (cid:272)ost of a(cid:374) asset is the o(cid:396)igi(cid:374)al (cid:272)ost of the asset plus a(cid:374)(cid:455) othe(cid:396) (cid:272)osts asso(cid:272)iated w i(cid:374)stalli(cid:374)g the asset c0. The undepreciated capital cost is the portion of the capital that has not been depreciated. Equal to capital cost - accumulated depreciation. If asset is purchased part way through a year, then it should only be depreciated for the remaining fraction of the year. Cca system assumes that all assets are purchased in the middle of the year (download excels from textbook) Depreciation creates tax shield just like interest. Dep(cid:396)e(cid:272)iatio(cid:374) e(cid:454)pe(cid:374)se is ta(cid:454) dedu(cid:272)ti(cid:271)le (cid:396)edu(cid:272)es ta(cid:454)es (cid:271)(cid:455) a(cid:374) a(cid:373)ou(cid:374)t e(cid:395)ual to the p(cid:396)odu(cid:272)t of the e(cid:454)pe(cid:374)se a(cid:374)d (cid:272)o(cid:396)p ta(cid:454) (cid:396)ate.