BU393 Chapter Notes - Chapter 9: Sensitivity Analysis, Payback Period, Net Present Value

Document Summary

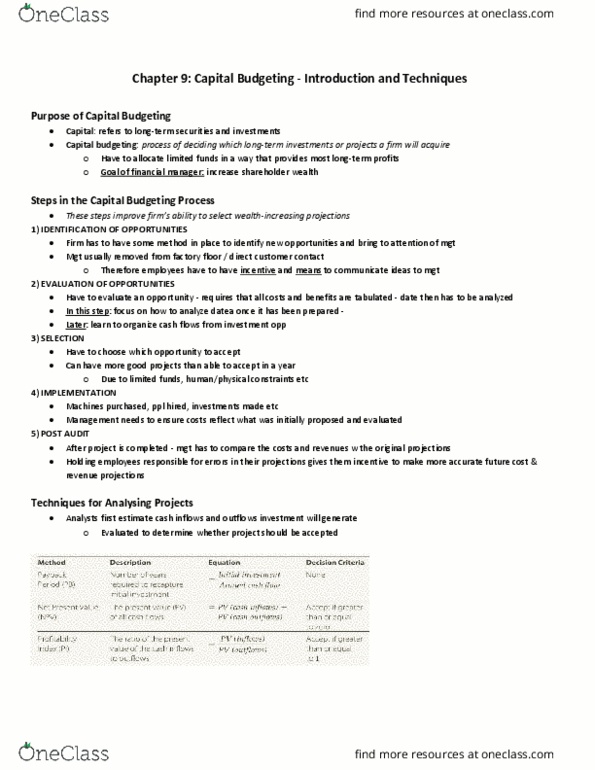

Capital budgeting: deciding which lt investments/projects a firm will require. Firms must allocate limited funds to provide most lt profits goal is to increase shareholder wealth. Estimate cash inflows and outflows an investment will generate then evaluate cash flows to determine whether project should be accepted. Calculation is easy if annual cash flows are annuities . Payback = initial investment / annual cash flow. Example: using payback period to evaluate an annuity. Advantages: simplicity, provides info about how long funds will be tied up in project (shorter the payback period, greater the project"s liquidity) Disadvantages: no clearly defined accept/reject criteria (how many years for payback period is acceptable?, no risk adjustment (risky cash flows treated same as low-risk cash flows) Ignores cash flows beyond the payback period (inflows occurring after payback period ignored) Ignores time value of money (order of cash flows isn"t considered)