BU387 Chapter Notes - Chapter 11: Market Capitalization, Capital Asset, Market Rate

Document Summary

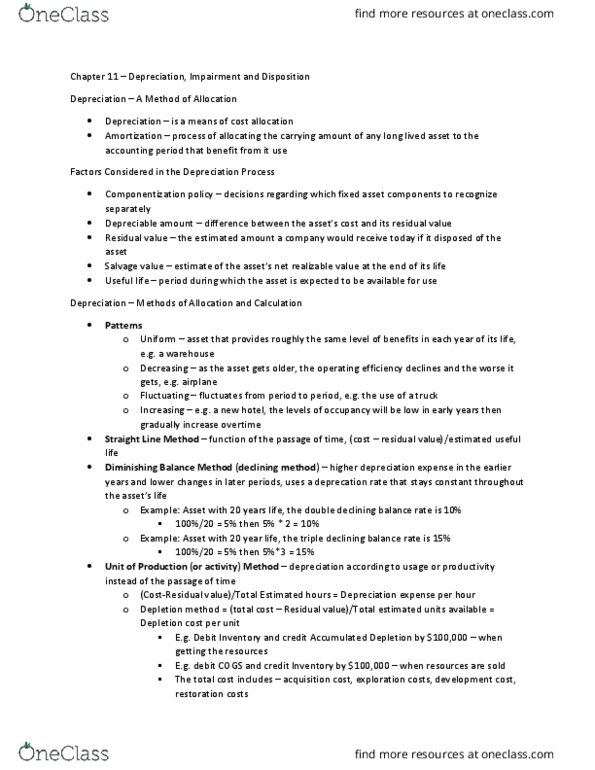

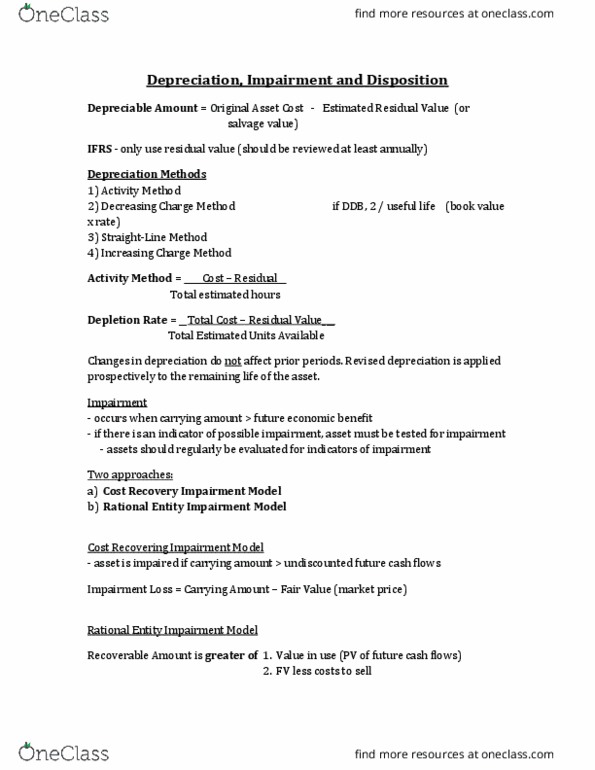

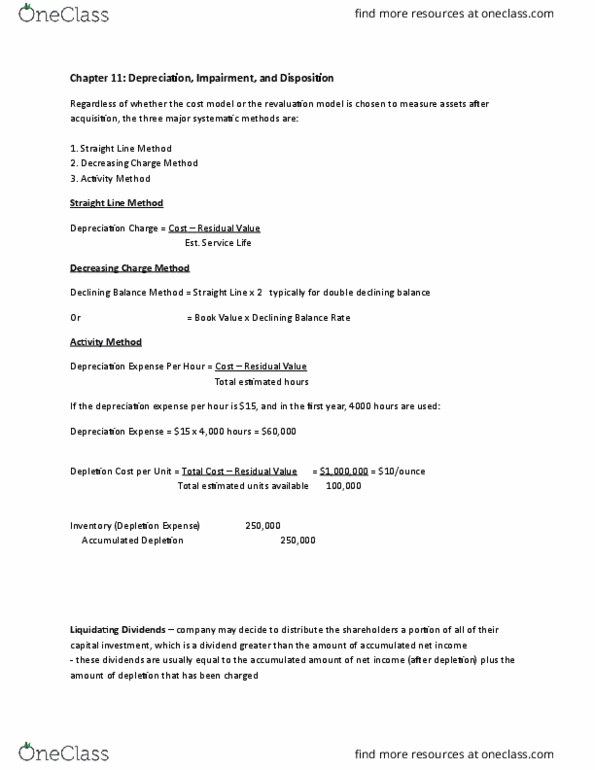

Important to consider because depreciation allocates the expenses of the asset with the revenue that it helped gain this also ensures that they do not pay a disproportionate amount in expenses in the year the asset was acquired. (2) depreciable amount: the amount is initially calculated as: original cost of asset minus estimated residual value, residual value = net amount expected to be received for the asset today at the condition the asset will be. ** so if you are given the straight line rate you can multiply it by 2 in order to get the double declining balance. Partial year depreciation: when an asset is acquired sometime during the year, a partial depreciation is taken, to do this, determine depreciation for a full year, allocate the amount between the two periods affected (multiply by the months) Asset will continue to be used in operations.