BU283 Chapter Notes - Chapter 6: Standard Deviation, Covariance, Systematic Risk

Document Summary

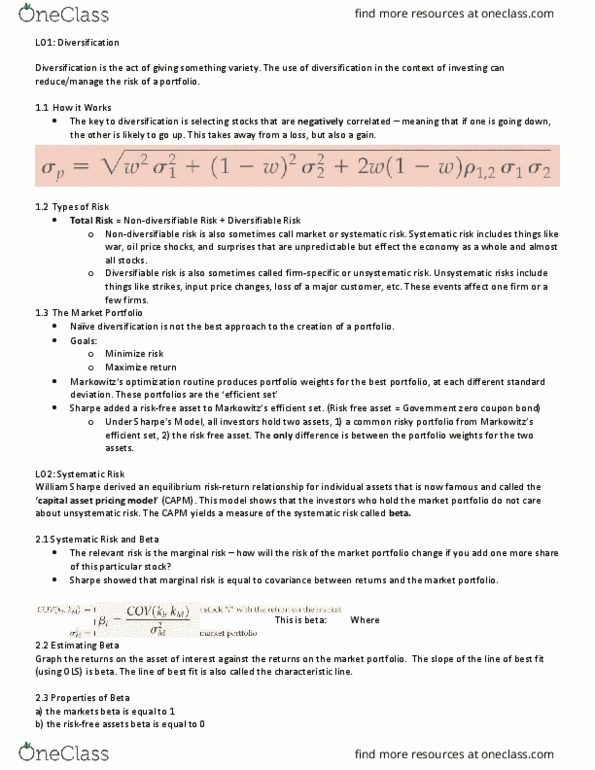

1. 1 how diversification works: portfolio standard deviation: true or false: a low-risk portfolio is constructed by selecting low-risk stocks, false. To build a low-risk portfolio, we collect stocks that are negatively correlated. As the number of stocks get very large (assuming equal weighting across stocks), the risk of each stock matters less and less and the variance of the portfolio converges toward the average of the pair-wise covariance"s. In other words, the risk is driven by the average degree of covariance. This result turns our intuition about portfolio risk upside down! It doesn"t matter how risky each of the stocks is. If you want to build a low-risk portfolio, then you pick stocks with low covariances (correlations) In reality, it is hard to find two stocks that are perfectly negatively correlated. But the good news is that diversification works as long as stocks are less than perfectly positively correlated.