BU247 Chapter Notes - Chapter 3: Variable Cost, Fixed Cost, Cost Driver

Document Summary

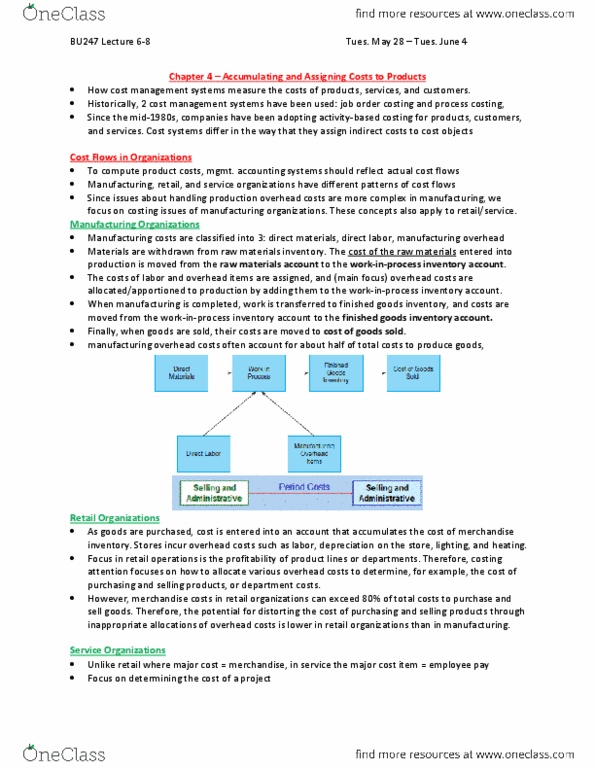

Chapter 3: accumulating and assigning costs to products. Cost flows in organizations to compute product costs, mgt accounting systems should reflect the actual cost flows in an organization. Manufacturing, retail + service organizations have different patterns of cost flows = different mgt accounting priorities. 3 groups: direct materials, direct labour, manufacturing overhead. Materials withdrawn from raw materials inventory as production begins. Costs are moved from raw materials account to work in process account. Manufacturing operation consumes labour and overhead items: costs added to work in process inventory. Manufacturing completed = costs transferred from work in process finished goods account: goods are finished + ready for sale. When goods are sold = costs moved from finished goods account on balance sheet to cost of goods sold on income. As goods purchased = costs entered into an account that accumulates cost of merchandise inventory in the store. Stores incur overhead costs like depreciation, lighting, labour, heating.