BU127 Chapter Notes - Chapter 10: Deferred Income, Contingent Liability, Current Liability

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

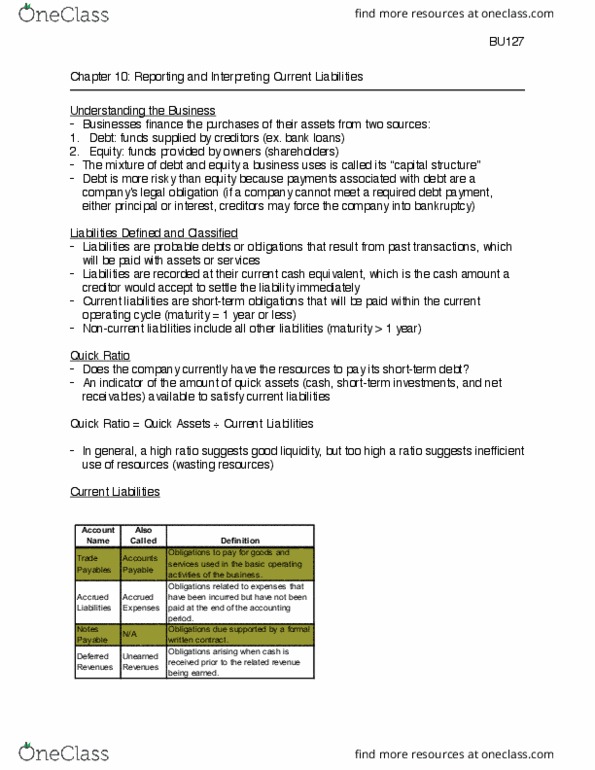

Bu127 chapter 10: reporting and interpreting current liabilities. Liabilities: debts/obligations arising from past transactions that will be paid with assets or services. Recorded at current cash equivalent cash amount a creditor would accept to settle the liability immediately. Interest payable in future isn"t included in amount of liability b/c it accrues and becomes liability with passage of time. Current liabilities: short-term obligations that will be paid within normal operating cycle or one year, whichever is longer. Companies that don"t settle current obligations in timely manner finds suppliers of g/s might not grant tem credit for purchases they have to seek short-term financing through banks. Use this ratio as indicator of amount of current assets available to satisfy current liabilities. High ratio suggests good liquidity but too high = inefficient use of resources. Used to recommend having ratios between 1 and 2 but now companies have under 1 since minimize funds invested in current assets.