BU127 Chapter Notes - Chapter 7: Gross Profit, Accounts Receivable, Internal Control

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

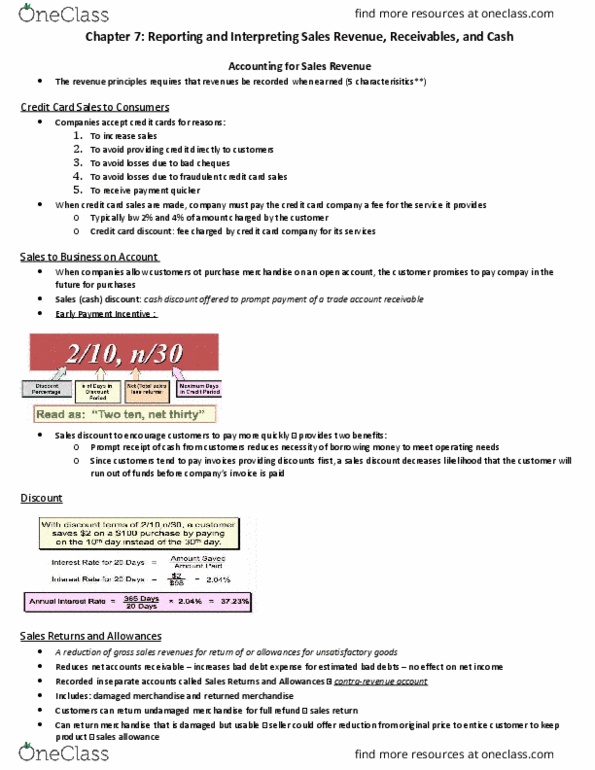

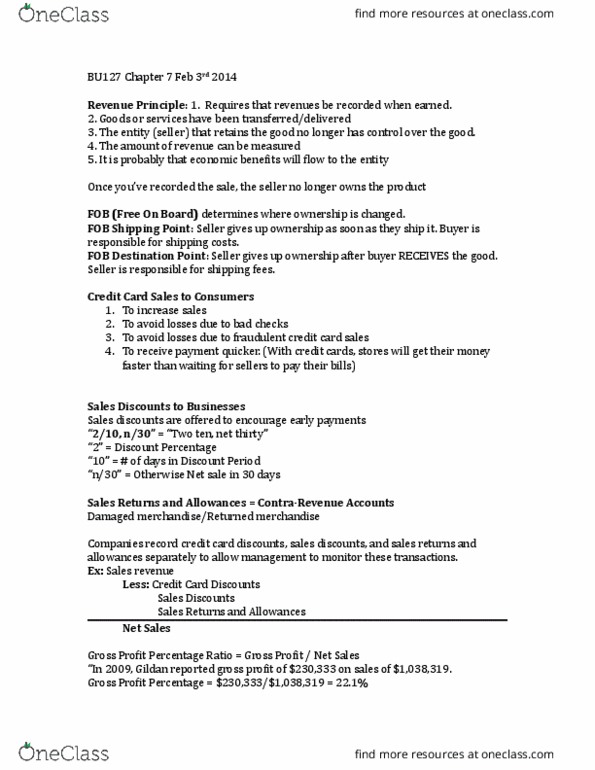

Chapter 7 reporting and interpreting sales revenue, The revenue principle requires that revenues be recorded when earned. The fee charged by the credit card company for its services is the credit card discount. A sales (or cash) discount is a cash offered to encourage prompt payment of a trade account receivable. Sales returns and allowances is a reduction of gross sales revenues for return of or allowances for unsatisfactory goods. Gross profit percentage is helpful in answering how effective the management is at selling goods and services for more than the costs to purchase or produce them. Trade receivables are open accounts owed to the business by trade customers and are created in the normal course of business when there is a sale of merchandise or services on credit. The allowance method bases bad debt expense on an estimate of uncollectible accounts. The first step is to estimate and record bad debt expenses.