Management and Organizational Studies 3363A/B Chapter Notes - Chapter 15: Analytical Review, Accounts Receivable, Gross Margin

21 Apr 2012

School

Department

Professor

Document Summary

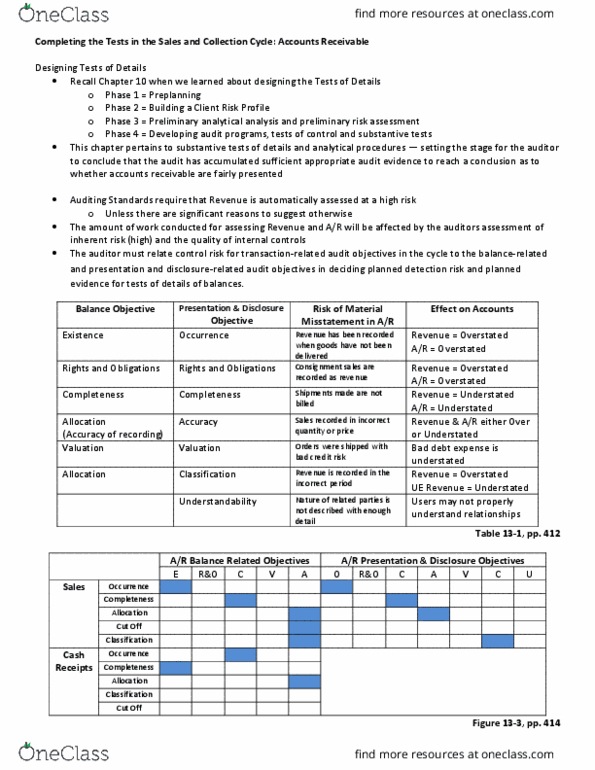

Review: pre- planning, client risk profile- preliminary analytical review, develop the strategic audit approach, develop audit programs, tests of controls, substantive tests. Tests of details of balances: ongoing evaluation, quality control and final evidence gathering, complete quality control and issue auditors report. Sales and collection cycle: transactions flow through accounts receivable are almost always material, unless collections are highly automated. Managers want accurate records to maintain good relationships with customers. If internal controls are weak, auditor will increase tests of details of balances. It is complicated because inherent and control risk both vary by objective. An evidence planning spreadsheet is used to determine the tests of details of balances (see p518 for example). Assess control risk- applied to sales and collections cycle in chapter 14. Identify at risk assertions- where substantive testing is insufficient. Design and perform tests of controls- chapter 14. Review large and unusual amounts, receivables from affiliated companies and related parties.