RSM324H1 Chapter Notes - Chapter 10: Student Loans In Canada, Unemployment Benefits, Canada Pension Plan

22 Feb 2017

School

Department

Course

Professor

Document Summary

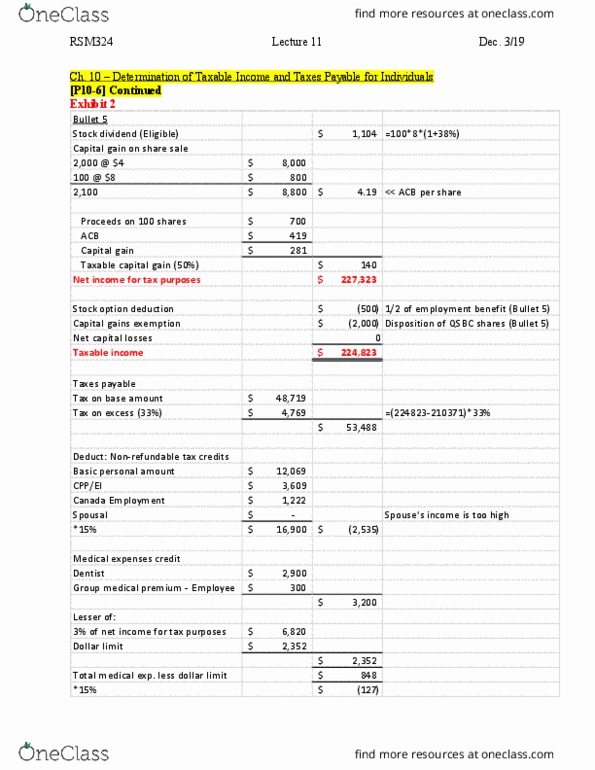

Chapter 10 individuals: determination of taxable income and taxes payable: medical expenses. E. g. , net income for tax purposes of ,000, the 15% credit can be applied only on medical expenses above ,200 (3% * ,000) The ,237 threshold occurs at net income of ,567 (3% * ,567) Taxpayers with net income above ,567 can deduct all medical expenses above ,237. The credit is available for medical expenses paid on behalf of the taxpayer, a spouse, or children under 18 at the end of the year. The tax credit for medical expenses paid for other dependents (children over 18) is 15% of the qualified medical expenses that exceed either 3% of the depe(cid:374)da(cid:374)t"s (cid:374)et i(cid:374)(cid:272)o(cid:373)e for the year, or ,237, whichever is less. Medical expenses qualifying for the credit include amounts paid in any 12- month period ending in the year: disability.