ECO105Y1 Chapter Notes - Chapter 6: Price Fixing, Economic Equilibrium, Order Of Newfoundland And Labrador

Document Summary

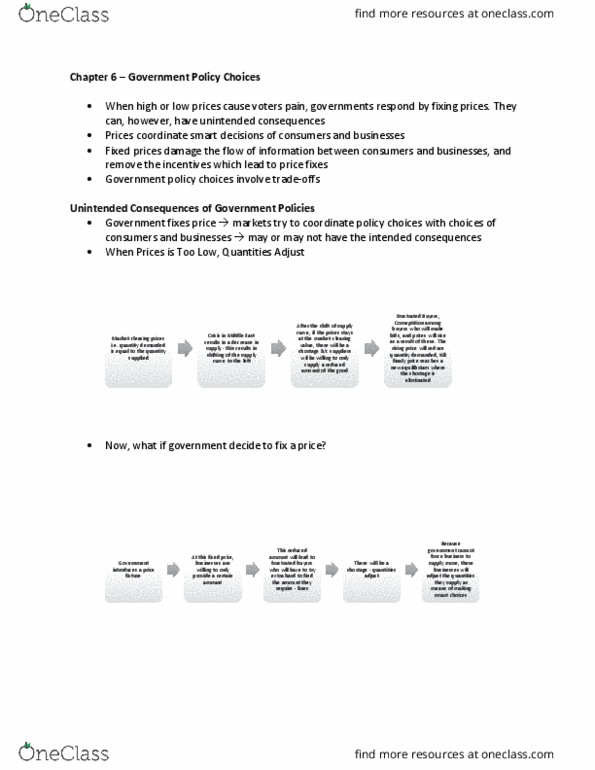

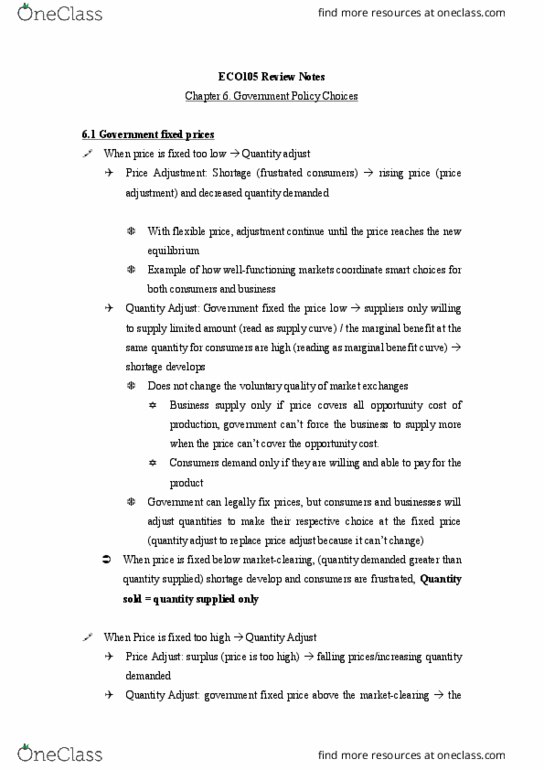

When price is fixed too low, quantities adjust. Prices adjust: frustrated buyers, consumers compete against each other for the now hard-to-find gasoline, and bid up prices. Flexible prices --> continue until the price reaches the new equilibrium price. Well-functioning markets coordinate smart choices for both consumers and businesses. Governments have the power to fix prices, but they can"t force businesses to produce if that price is not profitable. Consumers who are lucky enough to get the product at the fixed have a high opportunity cost (give up some driving) Fixing prices does not change the voluntary quality of market exchanges. Businesses supply only if price covers all opportunity costs of production. Consumers demand only if they are willing and able to pay for the product or service at that price. For any price --> businesses reduce output or shut down factories or move their inputs elsewhere. Consumers reduce their purchases or keep their wallets shut or buy something else (substitutes)