ECO101H1 Chapter Notes - Chapter 11: Average Variable Cost, Average Cost, Marginal Product

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

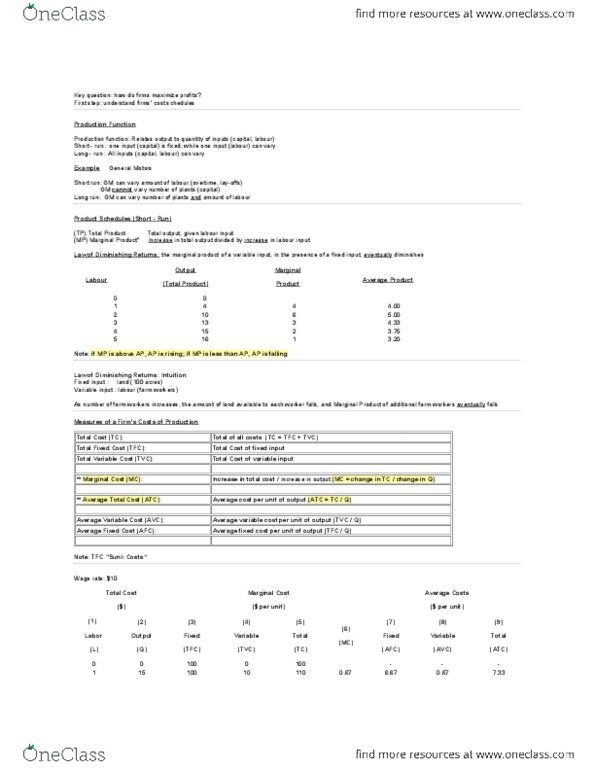

Production function: relationship between quantity of inputs and quantity of outputs. Short run: at least one input is fixed. Total product curve: shows relationship between output and a given variable input, with all other inputs fixed. Marginal product: additional quantity produced by adding one more unit of input. Marginal product of labour = change in qty of output / change in qty of labour. Average product: amount of output produced per input. Average product is maximized when average product equals marginal product. Variable cost: depends on the qty of output produced. Total cost curve: shows cost in relation to qty of output. Marginal cost curve: derivative of total cost curve. Average fixed cost: goes down as the cost is split up between more units of output. Average variable cost: usually goes up in direct correlation to output (relationship between variable cost and qty of output) Average total cost: amount of cost per unit of output (usually in a u shape)