AFM 361 Chapter Notes -Accounts Receivable, Capital Cost Allowance

15 Nov 2014

School

Department

Course

Professor

Document Summary

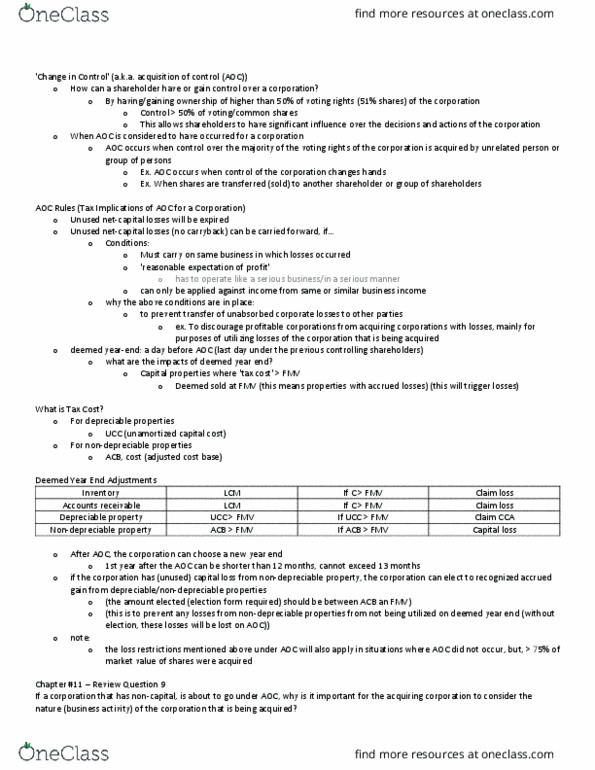

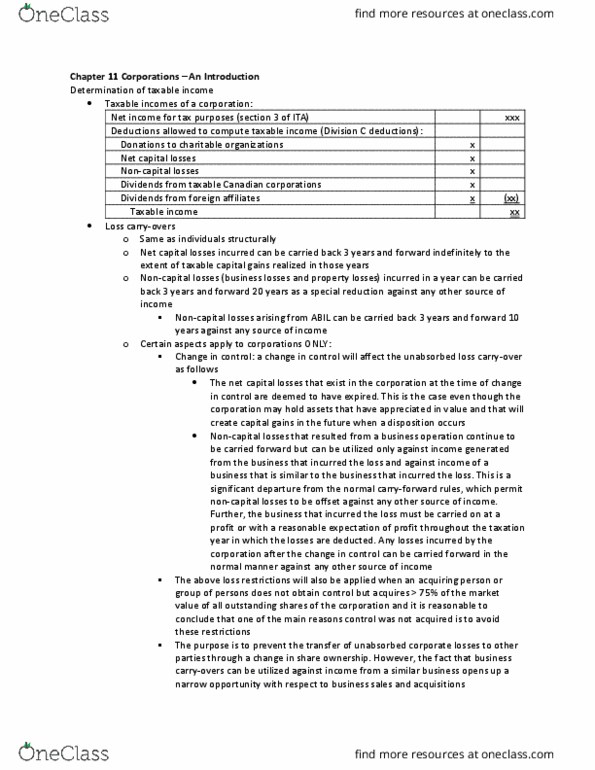

11,090 acquisition of control of a corporation and its effect on losses. For example, the assets of a profitable business or division in the income-generating corporation are transferred to the loss corporation. Usually the transfer will be accomplished by means of a tax free rollover by moving profit generating assets to the loss corporation. The income that is so generated is used to absorb the losses of the loss corporation: the second strategy involves implementing intercompany transactions which produce expense deductions to the income-generating corporation while generating income for the loss corporation. The upshot of this is that the normal 276 month (3 years back plus 20 years forward) carryover period for non-capital losses is reduced. This represents a constraint in that the corporation has a shorter period over which to generate income to utilize the losses. A short taxation year will also cause any capital cost allowance or small business deduction to be proportionately reduced.