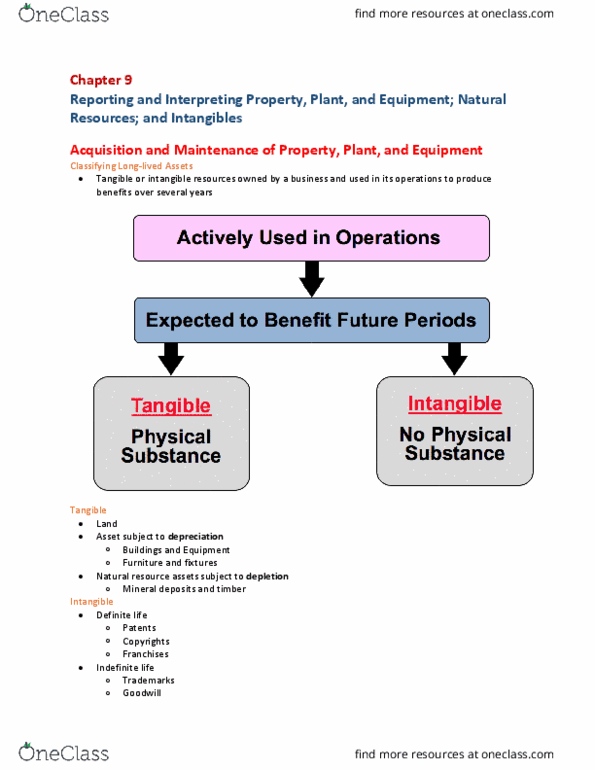

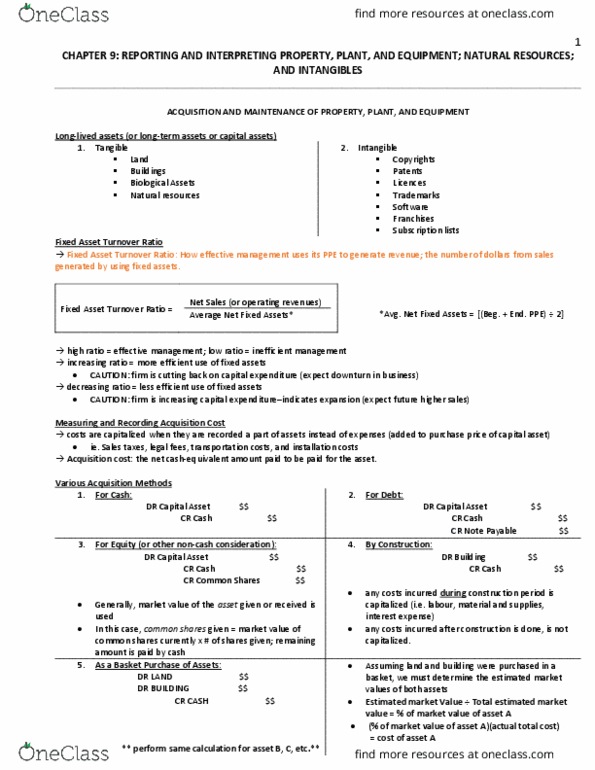

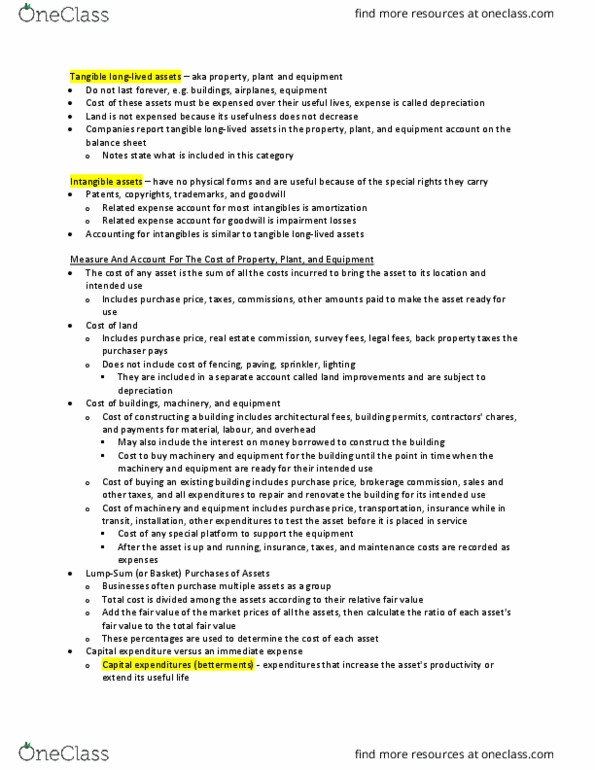

AFM101 Chapter 9: Chp9

AFM101 Full Course Notes

Document Summary

Get access

Related Documents

Related Questions

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2016. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.):

Depreciation is computed from the first of the month of acquisition to the first of the month of disposition.

Land A and Building A were acquired from a predecessor corporation. Thompson paid $812,500 for the land and building together. At the time of acquisition, the land had a fair value of $72,000 and the building had a fair value of $828,000.

Land B was acquired on October 2, 2016, in exchange for 3,000 newly issued shares of Thompsonâs common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $25 per share. During October 2016, Thompson paid $10,400 to demolish an existing building on this land so it could construct a new building.

Construction of Building B on the newly acquired land began on October 1, 2017. By September 30, 2018, Thompson had paid $210,000 of the estimated total construction costs of $300,000. Estimated completion and occupancy are July 2019.

Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $16,000 and the residual value at $2,000.

Machine Aâs total cost of $110,000 includes installation charges of $550 and normal repairs and maintenance of $11,000. Residual value is estimated at $5,500. Machine A was sold on February 1, 2018.

On October 1, 2017, Machine B was acquired with a down payment of $4,000 and the remaining payments to be made in 10 annual installments of $4,000 each beginning October 1, 2018. The prevailing interest rate was 8%.

Required:

Supply the correct amount for each answer box on the schedule. (Round your final answer to nearest whole dollar.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(LO 1) Darby Sporting Goods Inc. has been experiencing growth inthe demand for its products over the last several years. The lasttwo Olympic Games greatly increased the popularity of basketballaround the world. As a result, a European sports retailingconsortium entered into an agreement with Darby's RoundballDivision to purchase basketballs and other accessories on anincreasing basis over the next 5 years.

To be able to meet the quantity commitments of this agreement,Darby had to obtain additional manufacturing capacity. A realestate firm located an available factory in close proximity toDarby's Roundball manufacturing facility, and Darby agreed topurchase the factory and used machinery from Encino AthleticEquipment Company on October 1, 2016. Renovations were necessary toconvert the factory for Darby's manufacturing use.

The terms of the agreement required Darby to pay Encino $50,000when renovations started on January 1, 2017, with the balance to bepaid as renovations were completed. The overall purchase price forthe factory and machinery was $400,000. The building renovationswere contracted to Malone Construction at $100,000. The paymentsmade, as renovations progressed during 2017, are shown below. Thefactory was placed in service on January 1, 2018.

1/1 | 4/1 | 10/1 | 12/31 | |

Encino | $50,000 | $90,000 | $110,000 | $150,000 |

Malone | â30,000 | ââ30,000 | ââ40,000 |

On January 1, 2017, Darby secured a $500,000 line-of-credit witha 12% interest rate to finance the purchase cost of the factory andmachinery, and the renovation costs. Darby drew down on theline-of-credit to meet the payment schedule shown above; this wasDarby's only outstanding loan during 2017.

Bob Sprague, Darby's controller, will capitalize the maximumallowable interest costs for this project. Darby's policy regardingpurchases of this nature is to use the appraisal value of the landfor book purposes and prorate the balance of the purchase priceover the remaining items. The building had originally cost Encino$300,000 and had a net book value of $50,000, while the machineryoriginally cost $125,000 and had a net book value of $40,000 on thedate of sale. The land was recorded on Encino's books at $40,000.An appraisal, conducted by independent appraisers at the time ofacquisition, valued the land at $290,000, the building at $105,000,and the machinery at $45,000.

Angie Justice, chief engineer, estimated that the renovatedplant would be used for 15 years, with an estimated salvage valueof $30,000. Justice estimated that the productive machinery wouldhave a remaining useful life of 5 years and a salvage value of$3,000. Darby's depreciation policy specifies the 200%declining-balance method for machinery and the 150%declining-balance method for the plant. One-half year'sdepreciation is taken in the year the plant is placed in service,and one-half year is allowed when the property is disposed of orretired. Darby uses a 360-day year for calculating interestcosts.

Instructions

(a) Determine the amounts to be recorded on the booksof Darby Sporting Goods Inc. as of December 31, 2017, for each ofthe following properties acquired from Encino Athletic EquipmentCompany.

1.Land.

2.Buildings.

3.Machinery.

(b)

Calculate Darby Sporting Goods Inc.'s 2018 depreciation expense,for book purposes, for each of the properties acquired from EncinoAthletic Equipment Company.

(c)

Discuss the arguments for and against the capitalization ofinterest costs