AFM101 Chapter Notes - Chapter 2: Issued Shares, Current Liability, Intangible Asset

1 Feb 2014

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

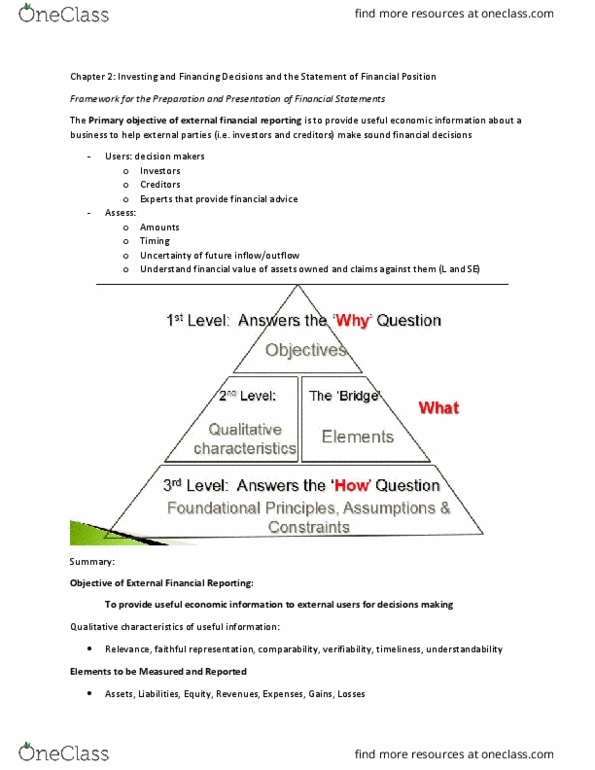

Chapter 2 investing and financing decisions and the statement of financial position. Objective of financial reporting to provide useful economic information about a business to help external parties, primarily investors and creditors, make sound financial decision in their capacity as capital providers. Three out of the four assumptions that underline accounting measurement and reporting relate to the statement of financial position. Separate-entity assumption states that business transactions are separate from the transactions of the owners. Unit of measure assumption states that accounting information should be measured and reported in the national monetary unit. The continuity (going-concern) assumption states that businesses are assumed to continue to operate into the foreseeable future. Cost principle requires assets to be recorded at the historical cash-equivalent cost, which is cash paid plus the current monetary value of all non-cash considerations also given in the exchange, on the date of transaction. Elements of the classified statement of financial position.