AFM101 Chapter Notes - Chapter 11: Private Placement, Current Liability, Debenture

26 Jun 2018

School

Department

Course

Professor

AFSA Education

Chapter 11 – Reporting and Interpreting Non-current Liabilities

- Non-Current Liabilities – all of the entity’s obligations not classified as current liabilities,

typically requires payment more than one year in the future

- Advantages of long term debt:

o Shareholders maintain control – debt does not dilute ownership and control of company

o Interest Expense is tax deductible – reduces net cost of borrowing

o The impact on earnings is positive – money can be borrowed on low interest rate

- Disadvantages:

o Risk of bankruptcy – interest payments must be made regardless if the company

generates net earnings or incurs a loss

o Negative impact on cash flows – debt must be repaid at a specific time

Characteristics of Long-Term Notes and Bonds Payable

- Private placement – when a company raises long term debt directly from financial service

organizations (banks, insurance companies, pensions fund companies, etc.)

o This debt is known as a note payable, which is a written promise to pay a stated sum of

money at one or more specified future dates, called the maturity dates

Bonds

- Bonds – publicly traded debt

- Lenders often protect their interests by requesting that the debt be secured rather than

unsecured

o Default – failure to make required payment

- A bond usually requires the payment of interest over its life, with the repayment of principal on

the maturity date

- Bond principal (aka par value, face amount, maturity value) – the amount payable at the

maturity of the bond. It is also the basis for computing periodic cash interest payments

o Can be any amount but it is usually $1000 for Canadian bonds

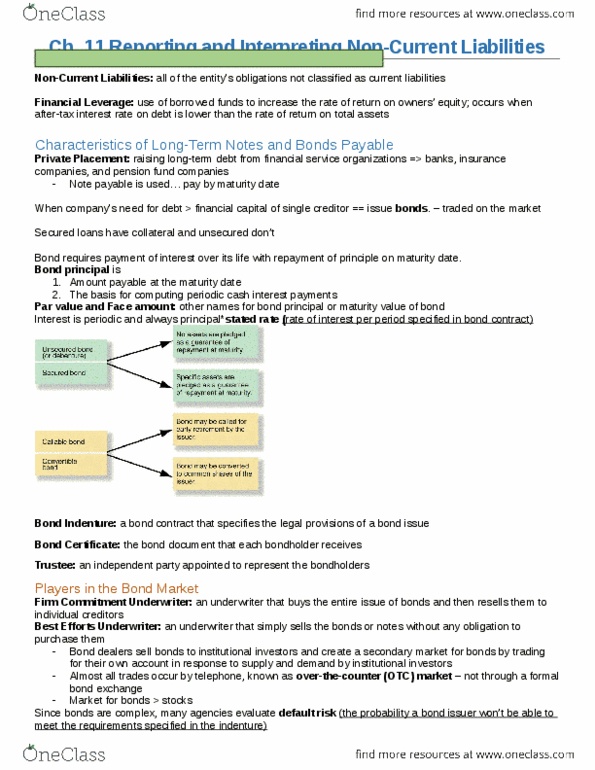

- Stated rate – the rate of interest per period specified in the bond contract

o Cash interest payments are usually annual or semi-annual

o Periodic interest payment = principal × stated rate

- The selling price of a bond does not affect the periodic cash payment of interest

- Different kinds of bonds have different characteristics:

o Debenture aka unsecured bond–no assets are specifically pledged to guarantee

repayment

o Secured bond – specific assets are pledged as a guarantee of repayment at maturity

o Callable bonds – may be called for early retirement at the option of the issuer

o Convertible bonds – may be converted to other securities of the issuer (usually common

shares)

- Indenture – a bond contract that specifics the legal provisions of a bond issue

o Includes maturity date, rate of interest to be paid, date of each interest payment, and

conversion privileges

o Also contains covenants to protect creditors

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Chapter 11 reporting and interpreting non-current liabilities. Non-current liabilities all of the entity"s obligations not classified as current liabilities, typically requires payment more than one year in the future. Advantages of long term debt: shareholders maintain control debt does not dilute ownership and control of company, the impact on earnings is positive money can be borrowed on low interest rate. Interest expense is tax deductible reduces net cost of borrowing. Disadvantages: risk of bankruptcy interest payments must be made regardless if the company generates net earnings or incurs a loss, negative impact on cash flows debt must be repaid at a specific time. Lenders often protect their interests by requesting that the debt be secured rather than unsecured: default failure to make required payment. A bond usually requires the payment of interest over its life, with the repayment of principal on the maturity date.