AFM101 Chapter Notes - Chapter 8: Inventory Turnover, High Tech, Perpetual Inventory

6 Dec 2016

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

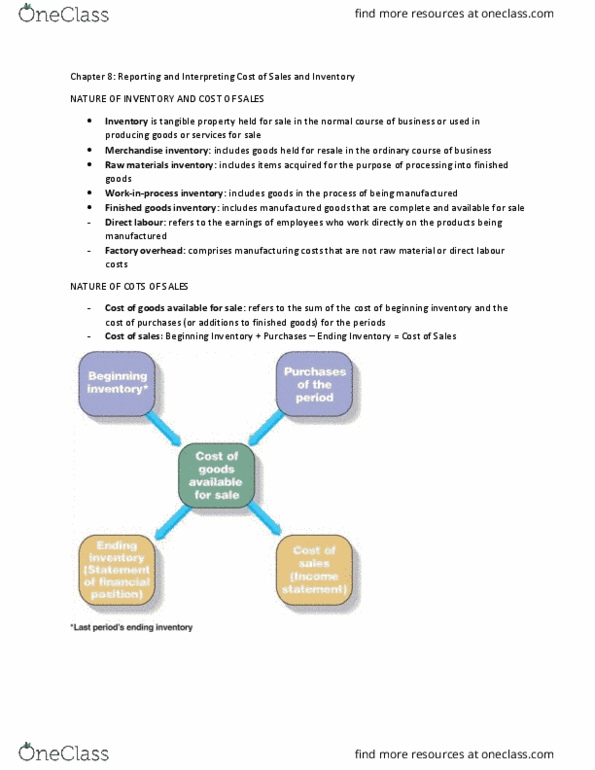

Chapter 8: reporting and interpreting cost of sales and inventory. You are responsible for appendix 8a (additional issues in measuring. Inventory: tangible property held for sale in the normal course of business or used in producing goods or services for sale. Merchandise inventory: includes goods held for resale in the ordinary course of business. Raw materials inventory: includes items acquired for the purpose of processing into finished goods. Work-in-process inventory: includes goods in the process of being manufactured. Finished goods inventory: consists of manufactured goods that are complete and available for sale. Fifo method: assumes that the oldest units (the first costs in) are the first units sold. Weighted-average cost method: uses the weighted-average unit cost of the goods available for sale for both cost of sales and ending inventory. Lifo: assumes that the most recently purchased items (the last ones in) are sold first and the oldest items are left in inventory.