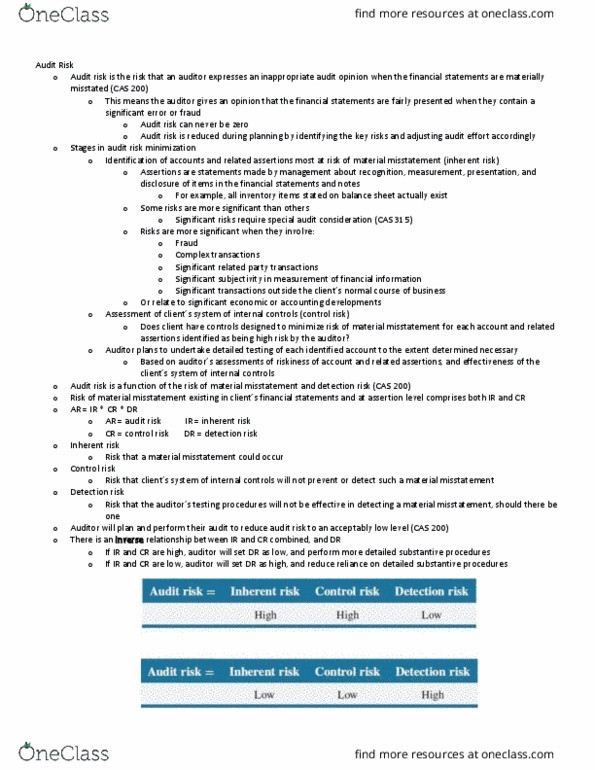

ADMN 4301H Chapter Notes - Chapter 6: Audit Risk, Audit Evidence, Internal Control

30 Mar 2020

School

Department

Course

Professor

Document Summary

Sampling is required whenever the auditor does not test an entire group of transactions or all items in a balance (cas 530) In many cases, there are too many items to test, or auditor decides that it is not necessary to test all items. Sample of items tested should be representative of the population. If sample contains fewer deviations than population, auditor over-relies on controls: concludes internal controls work effectively, audit is ineffective because risk of misstatement is greater than auditor"s assessment. If sample contains more deviations than population, auditor under-relies on controls: concludes internal controls do not work effectively, audit is inefficient because auditor does more work than necessary. If sample contains no material misstatements, auditor concludes financial statements not misstated when there is one in the population: audit is ineffective because risk of misstatement greater than auditor"s assessment. Spend too little time testing high risk accounts or critical controls.