BUS 426 Chapter Notes - Chapter 9: Audit Evidence, Risk Assessment, General Ledger

13 Nov 2016

School

Department

Course

Professor

Document Summary

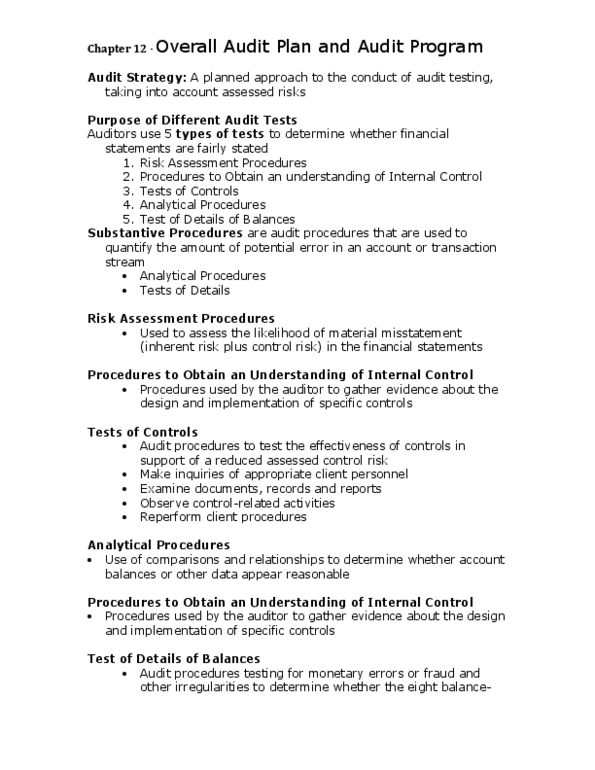

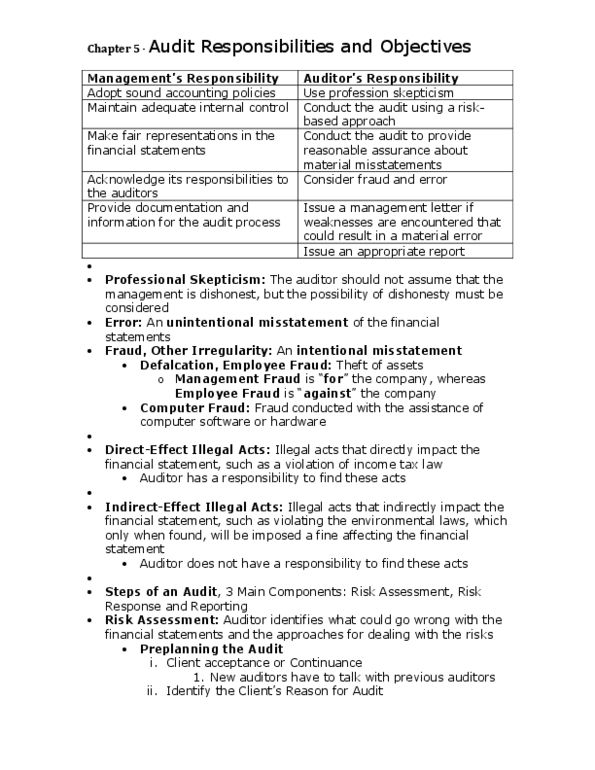

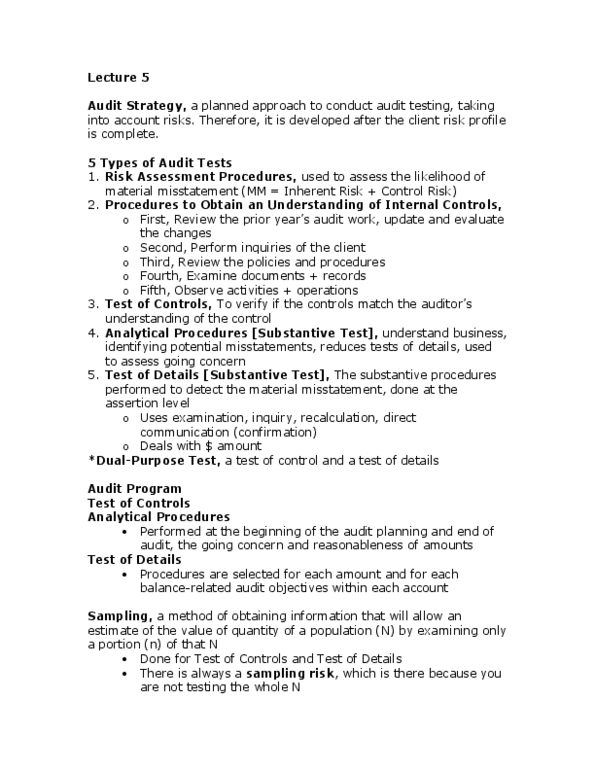

Risk assessment: to obtain information for identifying and assessing risks for material misstatement in the financial statements due to fraud or error, to plan audit procedure. Risk response: the actual audit procedures, tests of control. To test the effectiveness of control policies and procedures in support of a reduced assessed control risk: substantive procedures. To detect material misstatements in accounts, including tests of details and analytical procedures. Analytical procedures 3wevaluation of financial information through analysis of plausible relationships among financial and nonfinancial information. For each major class of transactions and material general ledger account, for each relevant assertion, the auditor looks at the potential for the risk of material misstatement. K(cid:374)o(cid:449)ledge of the (cid:272)lie(cid:374)t"s i(cid:374)dustr(cid:455), (cid:271)usi(cid:374)ess, a(cid:374)d operati(cid:374)g pro(cid:272)edures (cid:449)ill help the auditor complete the assessment. The detailed instructions for the collection of audit evidence. The actual task that you do to obtain evidence with respect to an audit objective.