SOC 103 Chapter Notes - Chapter 1: Embezzlement, Forensic Accountant, Internal Control

20 Dec 2016

School

Department

Course

Professor

Document Summary

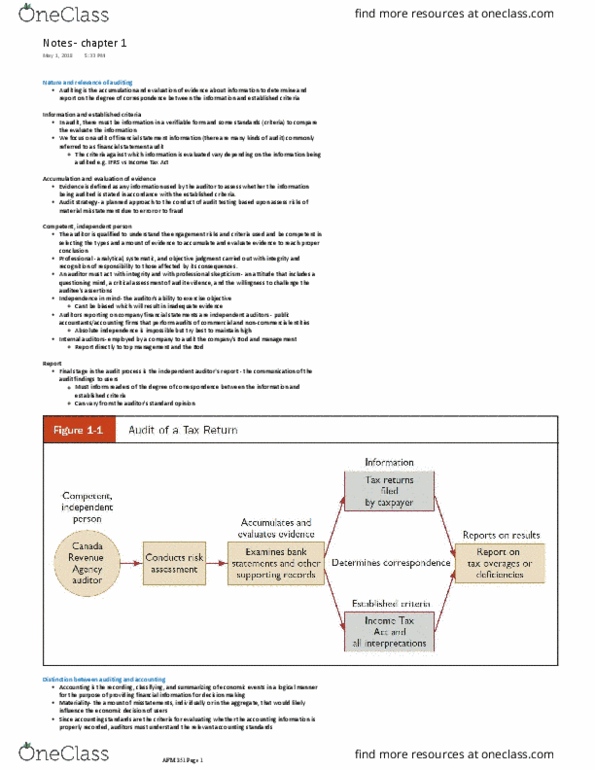

Chapter one: introduction to forensic accounting and fraud examination. Forensic accounting: is the application of investigative and analytical skills for the purpose of resolving financial issues in a manner that meets standards required by courts of law. Must meet courts of law that has jurisdiction. Fraud: is a result of misleading, intentional actions or inaction ( including making misleading statements and omitting relevant information) Fraud examination: includes services related to the purchase of businesses, valuation of divorce assets, determination of the dollar value of damages to business property, dispute resolutions and calculation of lost profits. Accounting: recording, classifying and summarizing economic events in a logical manner. Forensic accounting therefore refers to the use of accounting and information from other sources to objectively determine facts in a manner that can support reasonable positions taken in court. Tradition accounting: involves using financial language to communicate results of transactions and make decisions based on that communication.