ACC 406 Chapter Notes - Chapter 5: Income Statement, Cost Driver

28 Jun 2018

School

Department

Course

Professor

ACC – Chapter 5 – Job Order Costing

Firms producing unique products or services require a job-order accounting system

Firms in process industries mass-produce large quantities of similar or homogeneous products.

Process firms accumulate production costs by process or by department for a given period of

time

Job – one distinct unit or set of units

Job order costing system – where costs are assigned and accumulated by job

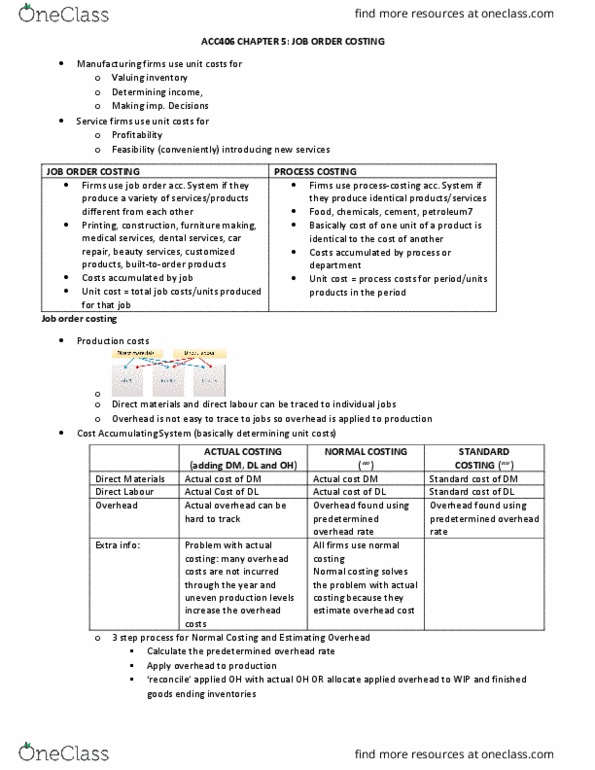

Two ways to measure the costs associated with production

Actual costing – requires the firm to use the actual cost of all direct materials, direct

labour and overhead used in production

oActual cost system

oRarely used because they cannot provide accurate unit cost information on a

timely basis

oMany overhead costs are not incurred uniformly throughout the year

oNonuniform production levels can mean that low production in one month

would give high unit overhead costs

Normal costing – requires firm to assign actual costs of direct materials and direct

labour to units produced and to apply overhead to units based on a predetermined

estimate

oNormal cost system

Normal costing and estimating overhead steps

1. Calculating predetermined overhead rate

Predetermined overhead rate – calculated at the beginning of the year by dividing

the total estimated annual overhead by the total estimated level of associated

activity or cost driver

Overhead rate = estimated annual overhead / estimated annual activity

2. Applying overhead to production

Applied overhead – found by multiplying the predetermined overhead rate by the

actual use of the associated activity for the period

3. Reconciling applied overhead with actual overhead or allocating applied overhead to

WIP and finished goods ending inventories

Underapplied overhead – if actual overhead is greater than applied overhead

oProduct cost has been understated

Overapplied overhead – if actual overhead is less than applied overhead

Plantewide overhead rate – a single overhead rate calculated by using all estimated overhead

for a factory divided by the estimated activity level across the entire factory

Departmental overhead rate – estimated overhead for a department divided by the estimated

activity level for that same department

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Acc chapter 5 job order costing. Firms producing unique products or services require a job-order accounting system. Firms in process industries mass-produce large quantities of similar or homogeneous products. Process firms accumulate production costs by process or by department for a given period of time. Job one distinct unit or set of units. Job order costing system where costs are assigned and accumulated by job. Two ways to measure the costs associated with production. Normal costing requires firm to assign actual costs of direct materials and direct labour to units produced and to apply overhead to units based on a predetermined estimate: normal cost system. Normal costing and estimating overhead steps: calculating predetermined overhead rate. Predetermined overhead rate calculated at the beginning of the year by dividing the total estimated annual overhead by the total estimated level of associated activity or cost driver. Overhead rate = estimated annual overhead / estimated annual activity: applying overhead to production.