ACC 406 Chapter Notes - Chapter 4: Contribution Margin, Earnings Before Interest And Taxes, Fixed Cost

1 Feb 2017

School

Department

Course

Professor

Document Summary

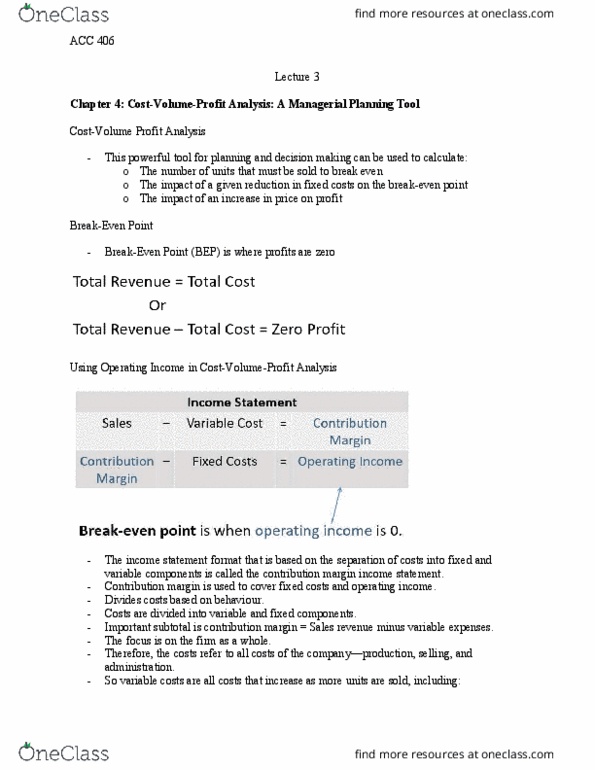

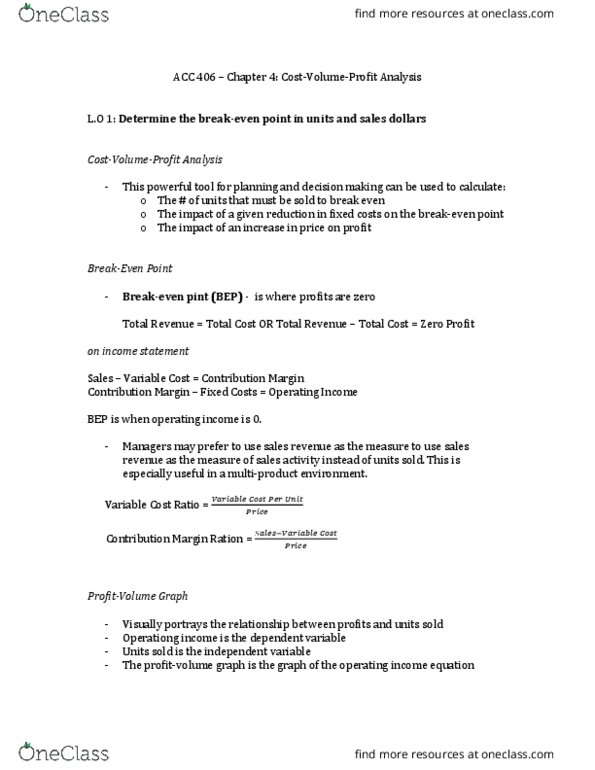

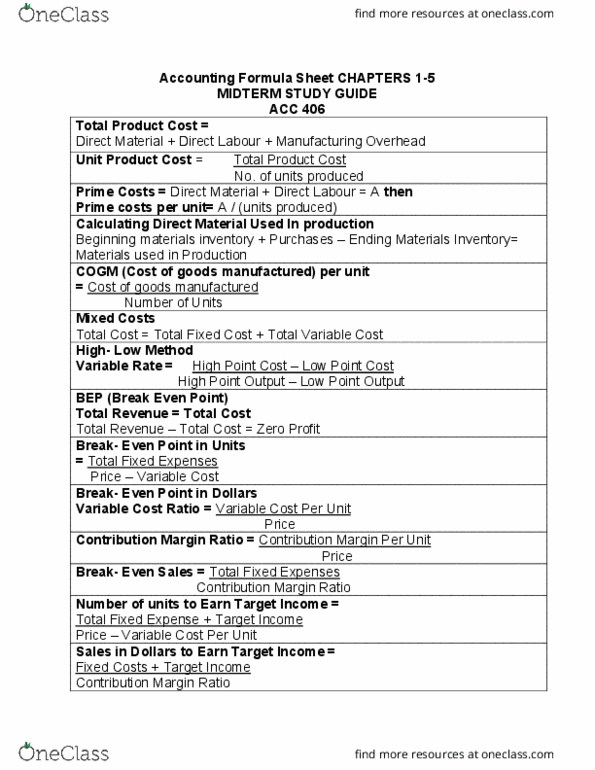

Chapter 4 cost, volu(cid:373)e, profit a(cid:374)alysis: a ma(cid:374)agerial. Break-even point in units and in sales dollars. Cost-volume-profit (cpv) analysis estimates how changes in cost (both variable and fi(cid:454)ed), sales (cid:448)olu(cid:373)e, a(cid:374)d p(cid:396)i(cid:272)e affe(cid:272)t a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s profit. The break-even point (bep) is the point where total revenue equal total cost. Fo(cid:396) cpv a(cid:374)al(cid:455)sis, it"s useful to o(cid:396)ga(cid:374)ize (cid:272)osts i(cid:374)to the fi(cid:454)ed a(cid:374)d (cid:448)a(cid:396)ia(cid:271)le (cid:272)o(cid:373)po(cid:374)e(cid:374)ts. Variable costs are all costs that increase as more units are sold, including: Fixed costs include fixed factory overhead and fixed selling and administrative costs. The i(cid:374)(cid:272)o(cid:373)e state(cid:373)e(cid:374)t fo(cid:396)(cid:373)at that"s (cid:271)ased o(cid:374) the sepa(cid:396)atio(cid:374) of (cid:272)osts i(cid:374)to fi(cid:454)ed a(cid:374)d variable components is called the contribution margin income statement. Defined as the excess of sales over variable costs. Contribution margin = sales variable costs. It"s useful (cid:271)e(cid:272)ause it p(cid:396)o(cid:448)ides i(cid:374)sight i(cid:374)to the p(cid:396)ofit pote(cid:374)tial of a (cid:272)o(cid:373)pa(cid:374)(cid:455). It indicates the percentage of each sales dollar available to cover the fixed costs and to provide income from operations.