ACC 100 Chapter Notes - Chapter 12: Cash Flow Statement, Current Asset, Income Statement

28 Jun 2018

School

Department

Course

Professor

ACC Chapter 12

Read page 570 - 577 (top), 593 - 596 (top)

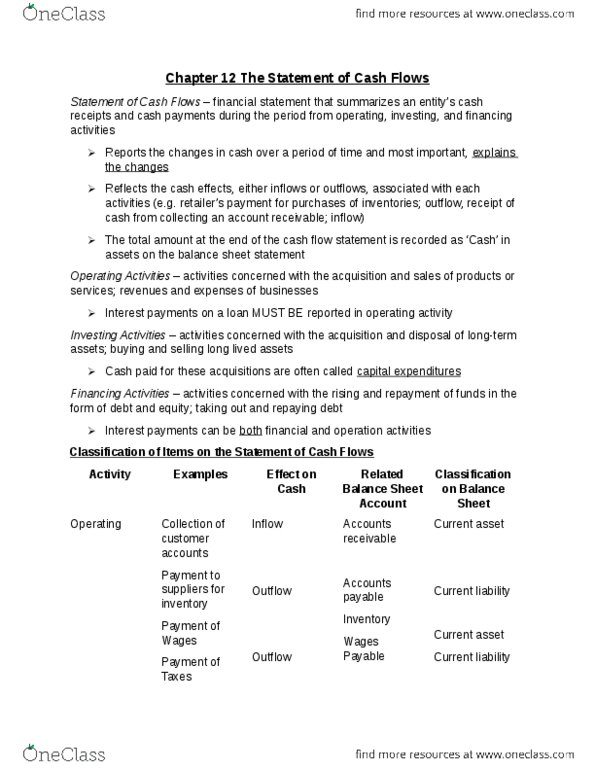

Statement of Cash Flows - the financial statement that summarized an entity’s cash

receipts and cash payments during the period from operation, investing and

financing activities

Changes in cash over a period of time and explains these changes

Complements the accrual-based income statement

On the statement

Cash provided (used) by operating activities

Cash provided (used) by investing activities

Cash provided (used) by financing activities

Net increase/decrease in cash

Cash balance at beginning of year

Cash balance at end of year

Purpose: to provide information about a company’s cash inflows and outflows

A cash equivalent is an investment that is readily convertible to a known amount of

cash and with a maturity to the investor of 3 months or less (combined with cash in

statement of cash flows)

Operating activities - acquiring and selling products and services

Cash flows from operating activities usually relate to an increase/decrease in

a current asset or liability

Investing activities - acquiring and disposing of long-term assets

Cash paid for these acquisitions is often called capital expenditures

Normally relate to long-term assets on the balance sheet

Financing activities - activities concerned with the raising and repayment of funds

in the form of debt and equity

Usually relate to long-term liabilities or shareholders equity

Cash from Operating Activities (CFO)

CFO is a key indicator as to whether the company’s normal operations have

generated sufficient cash flows to repay loans, maintain operating capability, make

new investments and provide distributions to the owners without having to rely on

external sources of financing

Negative CFO means that the operating activities are not producing enough cash to

cover the payments required by the process

The CFO section of a cash flow statement that uses the indirect method is especially

helpful in assessing the effects that changes in accruals and deferrals have on the

difference between accrual income and CFO

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Read page 570 - 577 (top), 593 - 596 (top) Statement of cash flows - the financial statement that summarized an entity"s cash receipts and cash payments during the period from operation, investing and financing activities. Changes in cash over a period of time and explains these changes. Purpose: to provide information about a company"s cash inflows and outflows. A cash equivalent is an investment that is readily convertible to a known amount of cash and with a maturity to the investor of 3 months or less (combined with cash in statement of cash flows) Operating activities - acquiring and selling products and services. Cash flows from operating activities usually relate to an increase/decrease in a current asset or liability. Investing activities - acquiring and disposing of long-term assets. Cash paid for these acquisitions is often called capital expenditures. Normally relate to long-term assets on the balance sheet.