ECON 1B03 Chapter Notes - Chapter 13: Marginal Product, Average Variable Cost

26 Jun 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

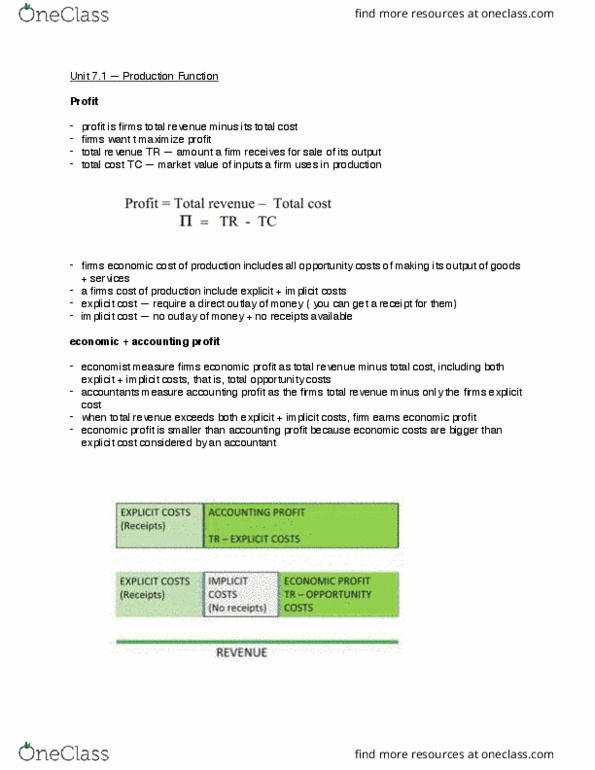

Chapter 13 costs of production: total revenue, tr, total cost, tc, profit = total revenue total cost. Economic profit = total revenue minus total cost, including both explicit and implicit costs, i. e. , opportunity costs. Accounting profit = total revenue minus only the firm"s explicit costs. Marginal product of any input in the production process is the increase in output that arises from an additional unit of that input. Mp is the slope of the total product function. Mp = change in total output = q change in # of inputs l . Diminishing marginal product is the property whereby the marginal product of an input declines as the quantity of the input increases. Tp is maximized when the slope of the tp function is zero. Since the slope of the tp function is mp, Ap tells us the quantity of output per input. Whenever mp > ap, ap must be increasing. Whenever mp < ap, ap must be decreasing.