16634 Chapter Notes - Chapter 1: Management Fee, Cash Flow, Gross Income

Document Summary

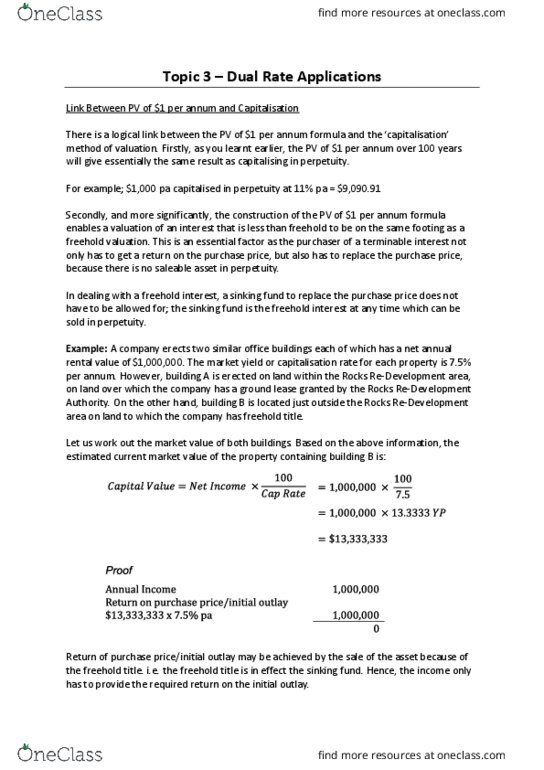

Capitalisation rate is the ratio between the net return and the property value it is the percentage return received from an income producing property. Gross income: is all income derived from an income producing property. Outgoings: are those expenditure items associated with the running of a property. Variations of the above formula allow valuers to determine the value of an income producing property: The te(cid:396)(cid:373) (cid:858)yea(cid:396)s pu(cid:396)(cid:272)hase(cid:859) (cid:396)efe(cid:396)s to the (cid:374)u(cid:373)(cid:271)e(cid:396) of yea(cid:396)s (cid:396)e(cid:395)ui(cid:396)ed fo(cid:396) the (cid:374)et (cid:396)etu(cid:396)(cid:374) f(cid:396)o(cid:373) the property (investment) to equal (replace) the purchase price. The number given once figures are put through the formula represents the time, in years, that it would take a property to pay for itself. The years purchase is the reciprocal of the capitalisation rate, and it can also be represented by the formula: Conversely, the capitalisation rate can be calculated through: If the cap rate changes then so does the yp and therefore the calculated value, demonstrated below: