21642 Chapter Notes - Chapter 8: Trend Analysis, Cl Financial, Market Price

13 Jun 2018

School

Department

Course

Professor

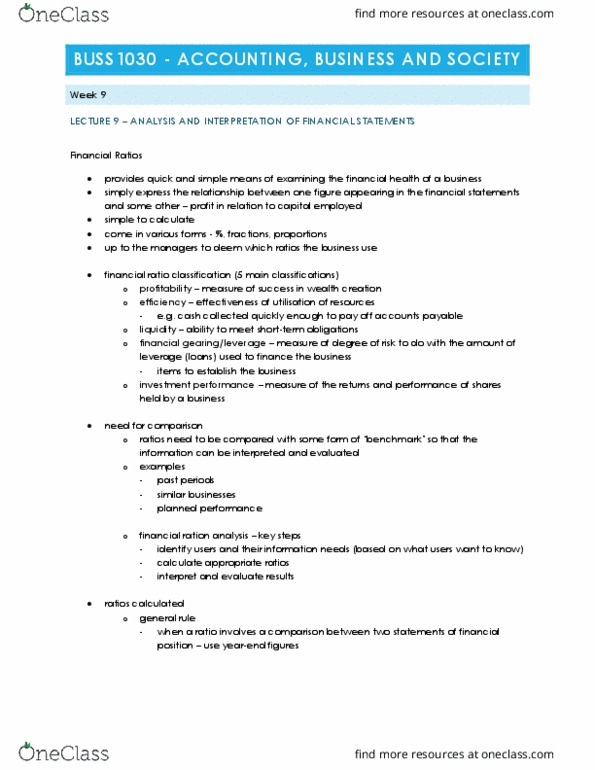

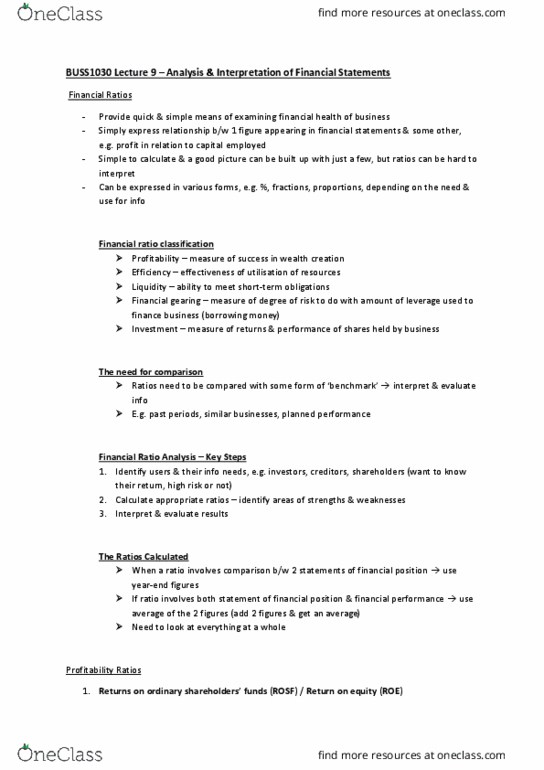

Analysis and Interpretation of Financial Statements

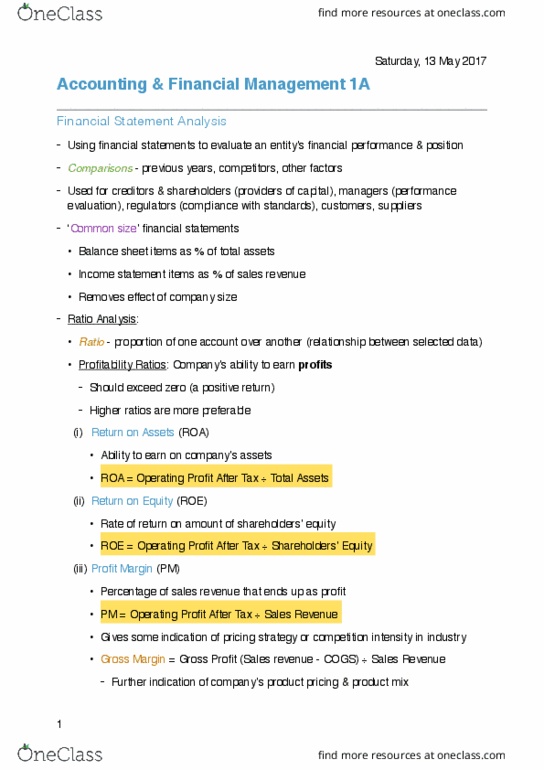

Objective of ratio analysis - to reveal the results of operations and finical conditions of a business.

Financial Ratios:

•Profitability - degree of financial success based on revenues and expenses

•Efficiency - how efficiently resources are being utilised

•Liquidity - how easily resources may be converted into cash

•Gearing - relationship between equity contributed by owners and by others

•Investment - assess the returns and performances of shares

Comparisons:

-Past periods

-Similar businesses

-Planned performance

Internal benchmarks:

-Budgets

-Previous results

-Other business units within the same firm

-Trends

External benchmarks:

-Competitors

-Industry averages

Key steps in financial ratio analysis:

1. Identify users and their information needs

2. Calculate appropriate ratios

3. Interpret and evaluate results

Average = Amount at start + End of year / 2

Profitability Ratios

Return on Equity (ROE) =

•Return on Shareholder’s Funds (ROSF) = Net profit after tax / Average shareholder’s equity x

100

•Return on Capital Employed (ROCE) = Earnings before interest and tax / Average shareholder’s

equity + Average long term equities x 100

•Earnings Before Interest and Tax (EBIT) Margin = EBIT / Sales x 100

EBIT = Operating Profit

•Gross Profit Margin = Gross profit / Sales x 100

find more resources at oneclass.com

find more resources at oneclass.com