BUSS1030 Chapter Notes - Chapter 1-13: Bitcoin, Risk Assessment, General Ledger

30 Jul 2018

School

Department

Course

Professor

Document Summary

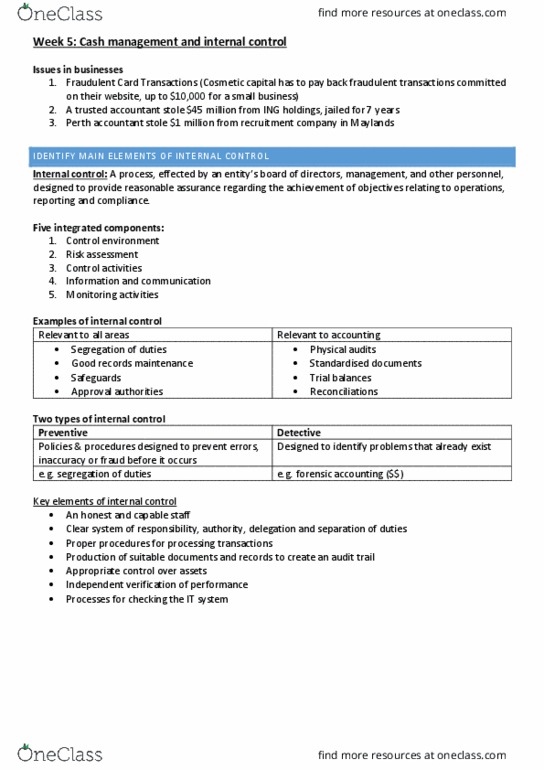

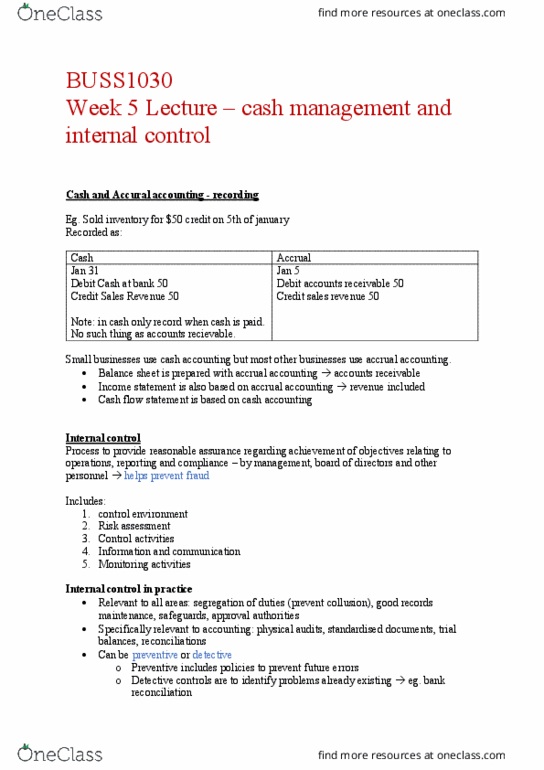

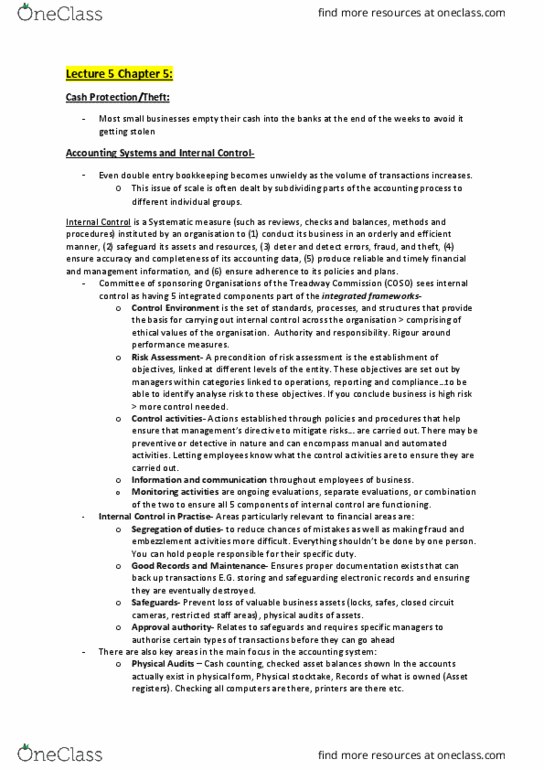

Chapter 5 cash management and internal control. Learning objective 1: identify the main elements of internal control and explain the need for sound internal control in accounting systems. Specifically relevant to accounting: physical audits inspection that assets will exist, standardized documents, trial balances, reconciliations. Internal controls can be preventative or detective: preventative policies/procedures designed to prevent errors, inaccuracy or fraud before it occurs, detective - designed to identify problems that already exist. E-commerce presents new challenges in internal control e. g. cryptocurrency (bitcoins) Internal controls need to be inter-organizational across organizations: electronic transactions do not have a paper trail cryptocurrency, tax, new elements of risk, lack of technical expertise, legal and technical issues. Internet is a public, rather than private, network intranet is private/internal. Any internal control system must consider cybersecurity: many issues are international, making consensus difficult, threats happening more quickly than regulations, e. g. stolen credit-card numbers, computer viruses and trojan horses, impersonation of companies.