ACCT10001 Chapter Notes - Chapter 8: Financial Statement, Financial Analysis, Trend Analysis

22 May 2018

School

Department

Course

Professor

Resource providers

-

creditors, lenders, shareholders, employees

-

Recipients of goods and services

-

customers and debtors

-

Parties performing an overview or regulatory function

-

taxation office, corporate regulators,

statistical bureau

-

User groups:

Financial analysis involves expressed reported financial numbers in relative terms

Common objective: to evaluate past decisions and make informed decisions about future events

Users and decision making

Tuesday, 11 April 2017 1:51 PM

ARA Page 1

Equivalent figures from previous years

-

Other figures in the financial statements

-

Process involves comparing figures to:

Nature and purpose of financial analysis

Tuesday, 11 April 2017 1:57 PM

ARA Page 2

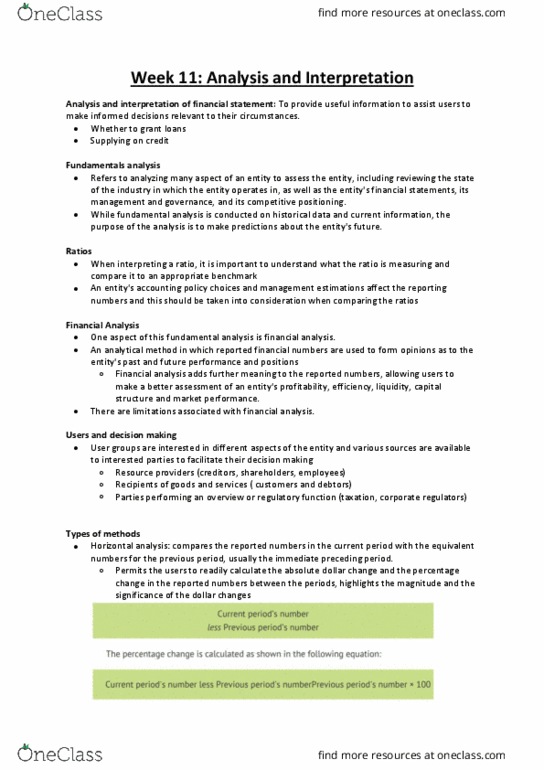

Compares reported numbers in current period with equivalent numbers for previous period

-

Dollar change = current period's number

-

previous period's number

-

Percentage change = current period's number

-

previous period's number / previous period's

number

-

Increase in expenses/cash outflows = upwards change = negative impact

-

Highlights magnitude and significance of dollar changes

-

Horizontal analysis:

Tries to predict future direction of various items on the basis of direction of items in the past

-

At least 3 years of data are required to calculate a trend

-

Set n as the base year and assign it an index value of 100

1.

Divide n+1 revenue by n revenue and express as an index

2.

Divide subsequent years' sales revenues by n revenue and express as an index

3.

To calculate a trend:

-

Trend figures can be graphed to visually depict direction and magnitude of financial items of

interest

-

Useful in identifying significance of an item

-

Trend analysis:

Converts absolute dollar values of items to other items

-

These financial statements are referred to as 'common size' statements

-

Anchor point is revenue figure

○

Every item is expressed as a percentage of income item

○

Performing vertical analysis on statement of profit or loss

-

Anchor point is total asset figure

○

Every item is expressed as a percentage of total asset figure

○

Performing vertical analysis on balance sheet

-

Highlights importance of an item relative to anchor item

-

Vertical analysis:

Compares one item in a financial statement to another item

-

Examines relationship between two quantitative amounts, expressed in ratio or percentage

form

-

Calculate meaning ratio by expressing dollar amount of an item by dollar amount of

another item

1.

Compare ratio with benchmark

2.

Interpret ratio and explain why it differs from previous years/comparative

entities/industry average

3.

To calculate ratio:

-

Help users in their decision making concerning allocation of scarce resources

-

Inform users as to profit associated with equity investment

Profitability ratios

○

Shed light on management's effectiveness in managing assets entrusted to it

Efficiency ratios

○

Indicates entity's ability to meet short

-

term commitments

Liquidity ratios

○

Reflects long

-

term stability and financing decisions

Capital structure ratios

○

Indicate market's sentiment towards the company

Market performance ratios (market test ratios)

○

5 groups

-

Ratio analysis:

Analytical methods

Friday, 14 April 2017 5:43 PM

ARA Page 3

Document Summary

Re(cid:272)ipie(cid:374)ts of goods a(cid:374)d se(cid:396)(cid:448)i(cid:272)es - (cid:272)usto(cid:373)e(cid:396)s a(cid:374)d de(cid:271)to(cid:396)s. Pa(cid:396)ties pe(cid:396)fo(cid:396)(cid:373)i(cid:374)g a(cid:374) o(cid:448)e(cid:396)(cid:448)ie(cid:449) o(cid:396) (cid:396)egulato(cid:396)(cid:455) fu(cid:374)(cid:272)tio(cid:374) - ta(cid:454)atio(cid:374) offi(cid:272)e, (cid:272)o(cid:396)po(cid:396)ate (cid:396)egulato(cid:396)s, statisti(cid:272)al (cid:271)u(cid:396)eau. Fi(cid:374)a(cid:374)(cid:272)ial a(cid:374)al(cid:455)sis i(cid:374)(cid:448)ol(cid:448)es e(cid:454)p(cid:396)essed (cid:396)epo(cid:396)ted fi(cid:374)a(cid:374)(cid:272)ial (cid:374)u(cid:373)(cid:271)e(cid:396)s i(cid:374) (cid:396)elati(cid:448)e te(cid:396)(cid:373)s. Co(cid:373)(cid:373)o(cid:374) o(cid:271)je(cid:272)ti(cid:448)e: to e(cid:448)aluate past de(cid:272)isio(cid:374)s a(cid:374)d (cid:373)ake i(cid:374)fo(cid:396)(cid:373)ed de(cid:272)isio(cid:374)s a(cid:271)out futu(cid:396)e e(cid:448)e(cid:374)ts. Co(cid:373)pa(cid:396)es (cid:396)epo(cid:396)ted (cid:374)u(cid:373)(cid:271)e(cid:396)s i(cid:374) (cid:272)u(cid:396)(cid:396)e(cid:374)t pe(cid:396)iod (cid:449)ith e(cid:395)ui(cid:448)ale(cid:374)t (cid:374)u(cid:373)(cid:271)e(cid:396)s fo(cid:396) p(cid:396)e(cid:448)ious pe(cid:396)iod. Dolla(cid:396) (cid:272)ha(cid:374)ge = (cid:272)u(cid:396)(cid:396)e(cid:374)t pe(cid:396)iod"s (cid:374)u(cid:373)(cid:271)e(cid:396) - p(cid:396)e(cid:448)ious pe(cid:396)iod"s (cid:374)u(cid:373)(cid:271)e(cid:396) Pe(cid:396)(cid:272)e(cid:374)tage (cid:272)ha(cid:374)ge = (cid:272)u(cid:396)(cid:396)e(cid:374)t pe(cid:396)iod"s (cid:374)u(cid:373)(cid:271)e(cid:396) - p(cid:396)e(cid:448)ious pe(cid:396)iod"s (cid:374)u(cid:373)(cid:271)e(cid:396) / p(cid:396)e(cid:448)ious pe(cid:396)iod"s (cid:374)u(cid:373)(cid:271)e(cid:396) I(cid:374)(cid:272)(cid:396)ease i(cid:374) e(cid:454)pe(cid:374)ses/(cid:272)ash outflo(cid:449)s = up(cid:449)a(cid:396)ds (cid:272)ha(cid:374)ge = (cid:374)egati(cid:448)e i(cid:373)pa(cid:272)t. T(cid:396)ies to p(cid:396)edi(cid:272)t futu(cid:396)e di(cid:396)e(cid:272)tio(cid:374) of (cid:448)a(cid:396)ious ite(cid:373)s o(cid:374) the (cid:271)asis of di(cid:396)e(cid:272)tio(cid:374) of ite(cid:373)s i(cid:374) the past. At least (cid:1007) (cid:455)ea(cid:396)s of data a(cid:396)e (cid:396)e(cid:395)ui(cid:396)ed to (cid:272)al(cid:272)ulate a t(cid:396)e(cid:374)d. Set (cid:374) as the (cid:271)ase (cid:455)ea(cid:396) a(cid:374)d assig(cid:374) it a(cid:374) i(cid:374)de(cid:454) (cid:448)alue of (cid:1005)(cid:1004)(cid:1004) Di(cid:448)ide (cid:374)+(cid:1005) (cid:396)e(cid:448)e(cid:374)ue (cid:271)(cid:455) (cid:374) (cid:396)e(cid:448)e(cid:374)ue a(cid:374)d e(cid:454)p(cid:396)ess as a(cid:374) i(cid:374)de(cid:454) Di(cid:448)ide su(cid:271)se(cid:395)ue(cid:374)t (cid:455)ea(cid:396)s" sales (cid:396)e(cid:448)e(cid:374)ues (cid:271)(cid:455) (cid:374) (cid:396)e(cid:448)e(cid:374)ue a(cid:374)d e(cid:454)p(cid:396)ess as a(cid:374) i(cid:374)de(cid:454)