ECON1101 Chapter Notes - Chapter 6: Diminishing Returns, Marginal Revenue, Marginal Cost

Chapter 6

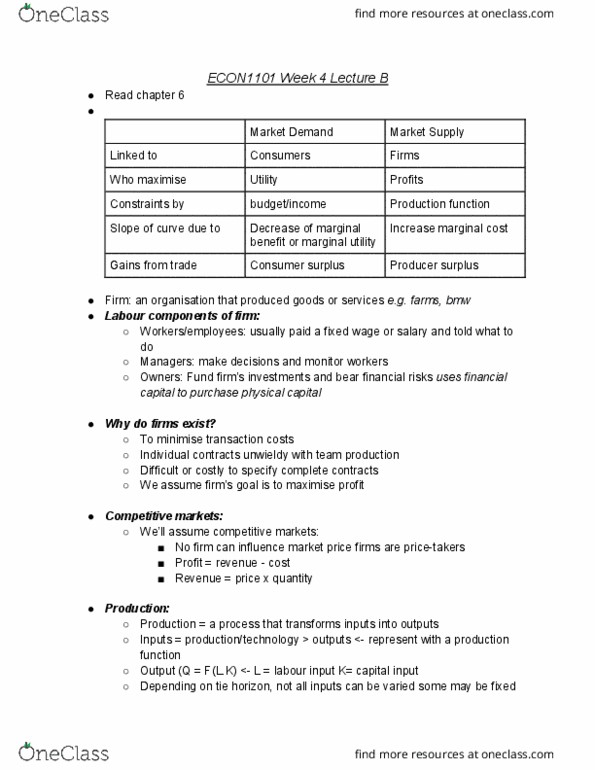

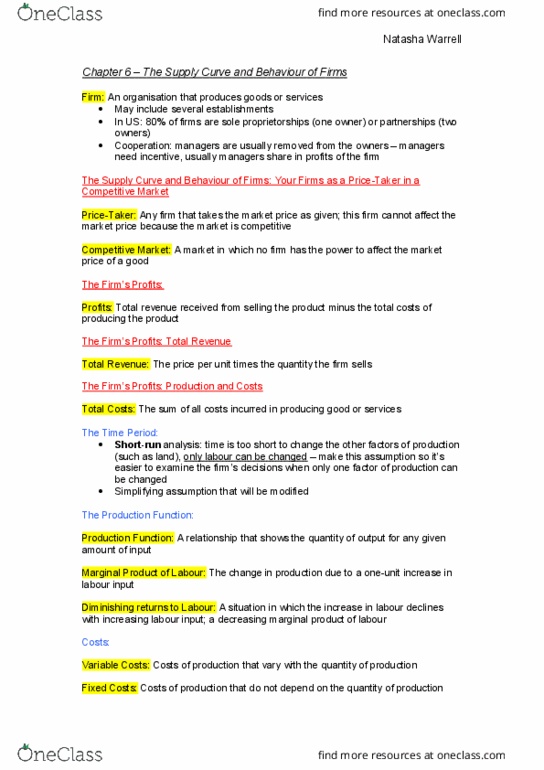

• Firm (company, business): organisation that produces goods and

services

o Labour components of firm:

▪ Workers/employees: usually paid a fixed wage or salary

and told what to do

▪ Managers: make decisions and monitor workers

▪ Owners: fund firm’s investments and bear financial risks

o Why do firms exist: (why do they not just get outside contractors)

▪ Minimize transaction costs (hire someone and when the

needs arise tell them what to do rather than → finding a

contractor, writing contract, etc.

▪ Individual contracts unwieldy with team production (team

needs to work well together)

▪ Difficult or costly to specify complete contracts

o We assume firm’s goal is to maximize profit

• Sole proprietor/ partnership: small number of owners, which manage

the firm

• Corporation: owners and managers have very little interaction

(managers have share in profits → incentive)

• Price taker: any firm that takes the market price as given; this firm

cannot affect the market price because the market is competitive

• Competitive market: a market in which no firm has the power to affect

the market price of any good

o At least seven firms competing with one another

o Individual firm demand is perfectly elastic at the market price

• Profits: total revenue – total costs (if equal → breaking even)

• Total costs: the sum of al costs incurred in producing goods and services

• Production function: a relationship that shown the quantity of output

for any amount of input

• Production: a process that transforms inputs to outputs

o Inputs production/ technology > output

o Output: Q = F (L , K)

o L= labour capital, K= capital input

o Depending on time horizon, not all inputs can be varied some may

be fixed

o Short run: some inputs are variable, all others fixed

• Marginal product of labor: the change in production due to a one- unit

increase in labour input

o Diminishing returns to labor: a situation in which the output due

to a unit increase in labor declines with increasing labor input

▪ Each worker has fewer tasks to do if the capacity of

factory/land is not increases → less additional output

o MPL = ∆Q/∆L roughly

• Variable costs: costs of production that vary with the quantity of

production

find more resources at oneclass.com

find more resources at oneclass.com