ECON1101 Chapter 10: ECON1101 Chapter 10

Natasha Warrell

Chapter 10 – Monopoly

A Model of Monopoly:

Monopoly: One firm in an industry selling a product that does not have close

substitutes

• Implicit in the definition of monopoly are barriers to entry – other firms are not

free to enter the industry

• The economist’s model of a monopoly assumes that the monopoly will

choose a level of output that maximises profits – the model of a monopoly is

like that of a competitive firm

• If increasing production will increase a monopoly’s profits, then the monopoly

will raise production – just as a competitive firm would

• The difference between a monopoly and a competitive firm: not what

motivates the firm but rather how its actions affect the market price

• MONOPOLY has market power

• MONOPOLY is a price-maker, competitive firms are price takers

Market Power: A firm’s power to set its price without losing its entire share of the

market

Price Maker: A firm that has the power to set its price, rather than taking the price set

by the market

Barriers to Entry: Anything that prevents firms from entering a market

E.g. De Beers created barriers to entry by maintaining exclusive rights to the

diamonds in most of the world’s diamond mines

Getting an Intuitive Feel for the Market Power of a Monopoly:

No One Can Undercut the Monopolist’s Price:

• When several sellers are competing with one another in a competitive market,

one seller can try to sell at a higher price, but no one will buy at that price

because another seller is always nearly who will undercut that price

• If a seller chargers at a higher price, everyone will ignore that seller; there is

no effect on the market price

• Monopoly’s situation is quite different:

▪ Instead of several sellers – the market has only one seller

▪ If the single seller sets a high price, it has no need to worry about

being undercut by other sellers

▪ There are no other sellers

▪ Therefore, the single seller – the monopoly – has the power to set a

high price

▪ The buyers probably will buy less at the higher price – this is, as the

price rises, the quantity demanded declines – but because no other

sellers offer that product or service, they probably will buy something

from the lone seller

The Impact of Quantity Decisions on the Price:

• Important difference between monopoly and a competitor: examine what

happens to the price when a firm changes the quantity is produces

▪ 100 firms in a market producing the same amount of bagels per day, if

one firm cuts its production the market price will rise by very little

(also, this price increase could motivate other firms to increase

Natasha Warrell

production slightly) – but overall impact on the price is negligible – no

power to affect the price

▪ Monopoly – is now the only firm in the market, if they were to cut

production the total quantity of product supplied to the market is cut in

half – big effect on the price in the market (immense power to affect

the price)

Showing Market Power with a Graph:

The Effects of Monopoly’s Decision on Revenues:

Total Revenue and Marginal Revenue:

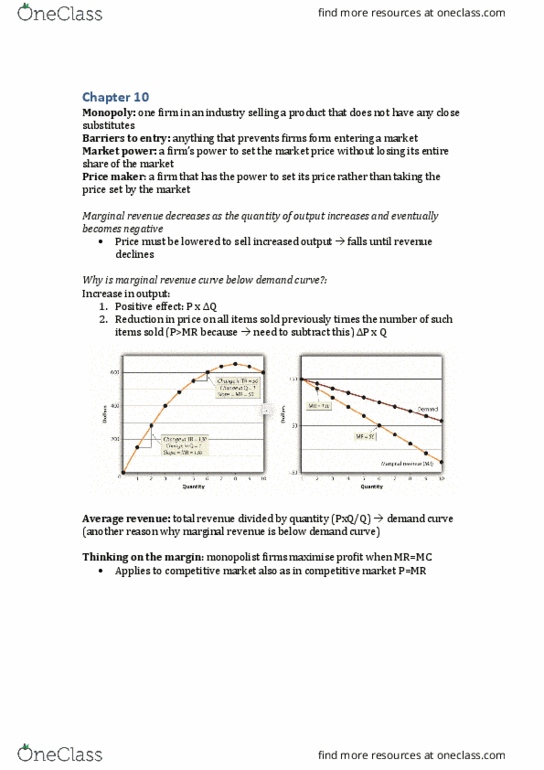

• Marginal revenue declines as the quantity of output rises and eventually

becomes negative – so although a monopolist has the power to influence the

price, this does not mean that it can get as high a level of total revenue as it

wants

• To sell more output – the monopolist must lower the price to get people to

buy the increased output, as it raises output it must lower the price more and

more – causing increase in total revenue to get smaller (as price falls to very

low levels revenue declines)

Total Revenue and Marginal Revenue:

• Marginal revenue is less than the price (except at the first unit of output,

where it equals the price)

• Marginal revenue curve lies below the demand curve

▪ Because when a monopolist increases output by one unit there are

two effects on total revenue:

1. A positive effect, which equals the price P times the additional

unit sold

2. A negative effect, which equals the reduction in the price on all

items previously sold times the number of such items sold (the

reduction in revenue due to the lower price on the items

previously produced)

▪ Second effect is subtracted from the first – therefore the price is

always greater than marginal revenue

Marginal Revenue and Elasticity:

Natasha Warrell

• Marginal revenue is negative when the price elasticity of demand is less than

one

• Monopolist would not produce so much that its marginal revenue was

negative – therefore concluded that a monopoly would never produce a level

of output for which the price elasticity of demand would be less than one

Average Revenue:

Average Revenue: Total revenue divided by quantity

• Use average revenue to show that marginal revenue is less than the price

• Total revenue equals price times quantity – average revenue = (P.Q)/Q = P

• Marginal must be less than the average (average declines) – therefore

because average revenues (prices) decline (demand curve slopes down) the

marginal revenue curve must lie below the demand curve

Finding Output to Maximise Profits at the Monopoly:

• A monopolist will never produce a quantity for which marginal revenue is

negative but that does not mean that it will produce until marginal revenue is

0 – if each additional unit brings in extra revenue the firm will have to look at

the costs of producing that extra unit as well

• Total costs increase as more is produced (at least for high levels of output)

• Marginal costs increases as more is produced (at least for high levels of

output)

Comparing Total Revenue and Total Costs:

• Difference between total revenue and total costs is profits

• Quantity produced increases → both total revenue from selling the product

and the total costs of producing the product increase – eventually profits must

reach a maximum

• Profits are shown as the gap between total costs and total revenue (graph)

Equating Marginal Cost and Marginal Revenue:

• If marginal revenue is greater than the marginal cost of the additional unit –

profits will increase if the unit is produced (therefore should be produced –

total revenue rises more than total costs)

• Monopolist should increase its output as long as marginal revenue is greater

than marginal cost – marginal revenue is decreasing so at some level of

output marginal revenue will drop below marginal cost

• Monopolist should produce up to the level of production where MC = MR

MC = MR at a Monopoly versus MC = P at a Competitive Firm:

Marginal Revenue Equals the Price for a Price-Taker:

• For a competitive firm: total revenue = PQ

• Competitive firm can not affect the price – therefore when the quantity sold is

increased by one unit, revenue is increased by the price (marginal revenue

equals the price for a competitive firm)

• MC = MR rule applies to both monopolies and competitive firms that

maximise profits

A Visual Comparison:

• Monopoly total revenue curve: turn down at higher levels of output