ACC101 Chapter chapter 1: INTRODUCTION TO ACCOUNTING

Document Summary

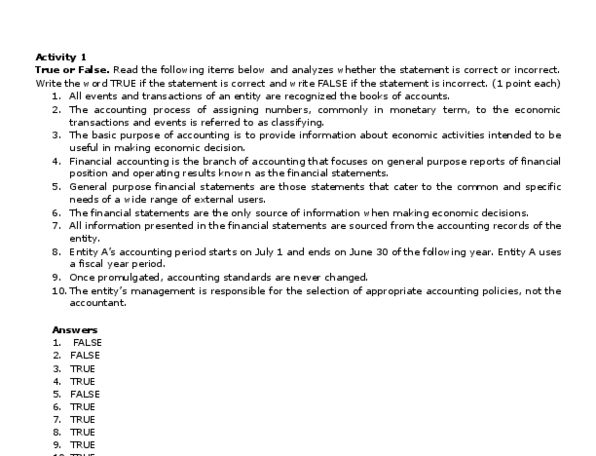

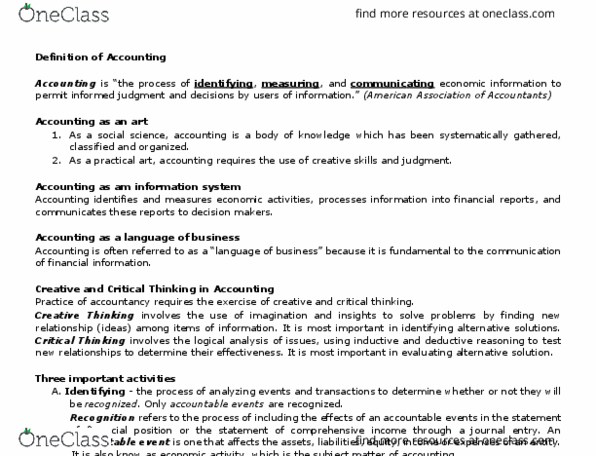

Accounting is a process of identifying, recording and communicating economic information that is useful in making economic decisions. Essential elements: identifying the accountant analyzes each business transaction and identifies whether the transaction is an accountable event or not. Only accountable events are recorded in the book of accounts. Accountable events or economic events are those that affect the assets, liabilities, equity, income and expenses: recording- the accountant records the economic events he has identified. This process is called journalizing: communicating at the end of each accounting period, the accountant summarizes the information processed in the accounting system in order to produce meaningful reports. (financial statements) Types of information: quantitative information expressed in numbers and quantities, qualitative information expressed in words or descriptive form, financial information expressed in money. Can be viewed as quantitative information because monetary amounts are expressed in numbers.