MGT 210 Lecture 9: Chapter 9

Document Summary

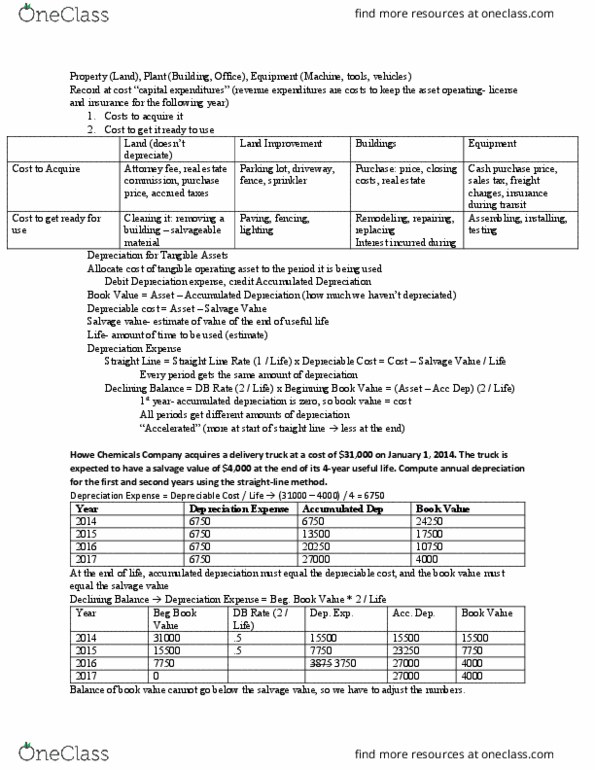

Cost = all expenditures necessary to acquire an asset and make it ready to use. Plant asset- resources that have physical substance that are used in the operations of a business (property, plant, and equipment) Except for land, plant assets depreciate over their useful lives. Must keep assets in good condition, replace worn-out assets, and expand productive assets as needed. Historical cost principle- all plant assets recorded at cost. Revenue expenditures- costs not included in the plant asset account (immediate expense) Capital expenditure- costs included in plant asset account (not expensed until later) Cost measured by cash equivalent price- fair value of asset given up/received. Cost = cash purchase price + closing costs (title and attorney"s fees) + real estate commissions +accrued property taxes from the previous owner. All costs incurred in making land ready to use increased (debit) the land account. Company acquires land costs include clearing, draining, filling, and grading.