ECON 203 Lecture Notes - Lecture 1: Statistical Model

Document Summary

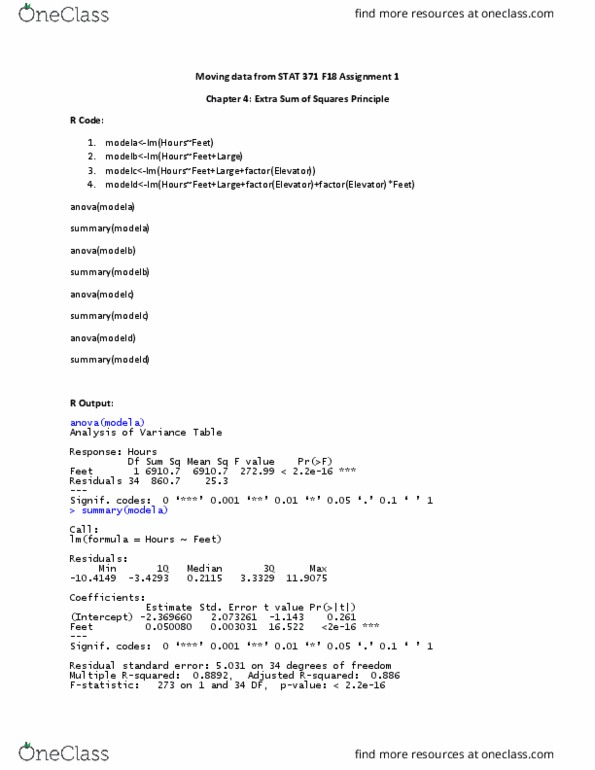

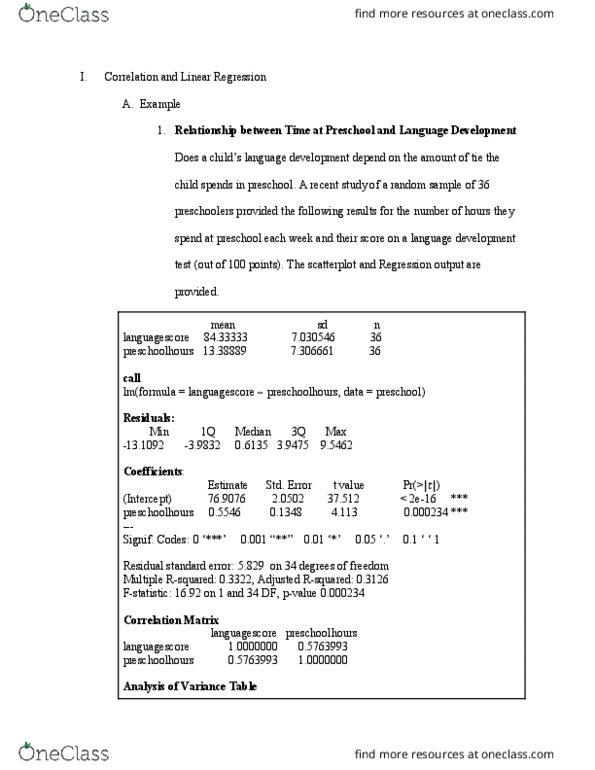

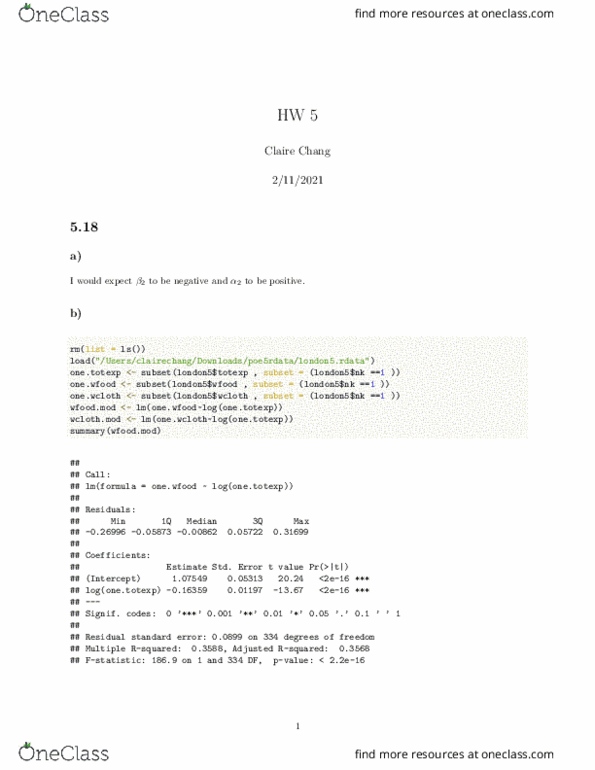

Benchmark model- how well does the market predict payoff (last vs. actual) Error t value pr(>|t|) (intercept) 2. 99303 0. 17989 16. 64 <2e-16 *** Residual standard error: 4. 292 on 1860 degrees of freedom. F-statistic: 1381 on 1 and 1860 df, p-value: < 2. 2e-16. R2 = 42. 62% - as we can see from the graph, the market does not predict the payoff accurately based on the last price of the option. How well the expected payoff mimics the last price (exp_payoff vs last) Error t value pr(>|t|) (intercept) 0. 717374 0. 074559 9. 622 <2e-16 *** exp_payoff 0. 780406 0. 009946 78. 461 <2e-16 *** Residual standard error: 1. 786 on 1860 degrees of freedom. F-statistic: 6156 on 1 and 1860 df, p-value: < 2. 2e-16. R2 = 76. 8% the data points fit the trendline much better in this example. The option price generated by the model fits the market price quite well. Error t value pr(>|t|) (intercept) 2. 43017 0. 17170 14. 15 < 2e-16 ***