ECON 101 Lecture 14: Lecture 14: Firms and Production

30

ECON 101 Full Course Notes

Verified Note

30 documents

Document Summary

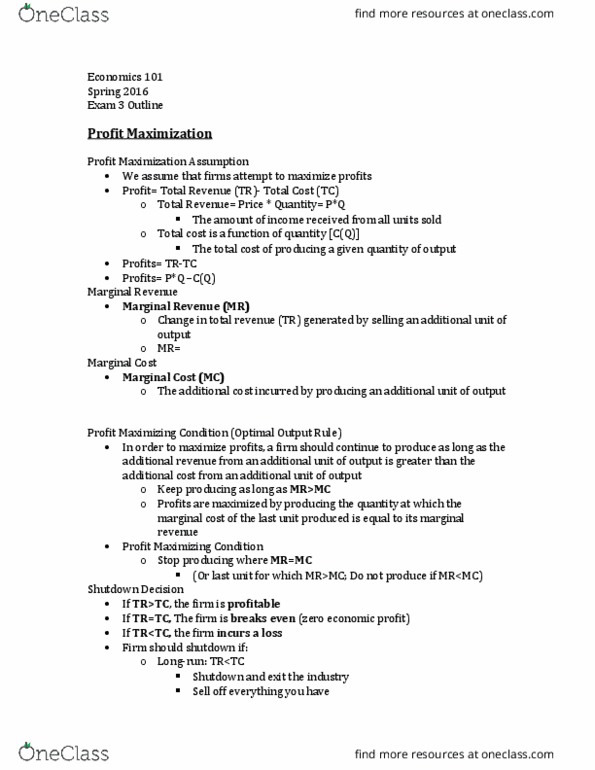

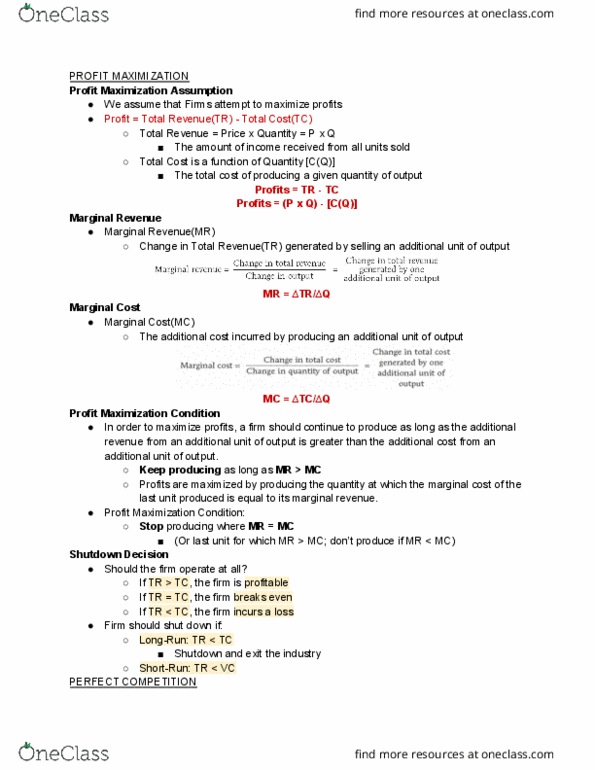

An entity that converts inputs into outputs. Capital: durable goods used in the production of other goods. Outputs: goods or services sold to consumers. Firms owned and operated by a single individual. 72% of firms, 4% of sales (statistical abstract of the united states) Firms jointly owned and controlled by two or more people. Firms owned by shareholders in proportion to number of shares of stock they hold. We assume that firms attempt to maximize profits. Profit = total revenue (tr) - total cost (tc) Total revenue = price x quantity = p*q. You"re assuming that for every quantity you sell, you"re selling it for the same price. Total cost is a function of quantity [c(q)] May balance profits against leisure time, other activities. May maximize something else - output, revenue. In order to maximize profits the firm must produce a given quantity as efficiently as possible. Getting most output possible from a given set of inputs.