ECON 102 Lecture Notes - Lecture 16: Fixed Cost, Marginal Product

17 Dec 2015

School

Department

Course

13

ECON 102 Full Course Notes

Verified Note

13 documents

Document Summary

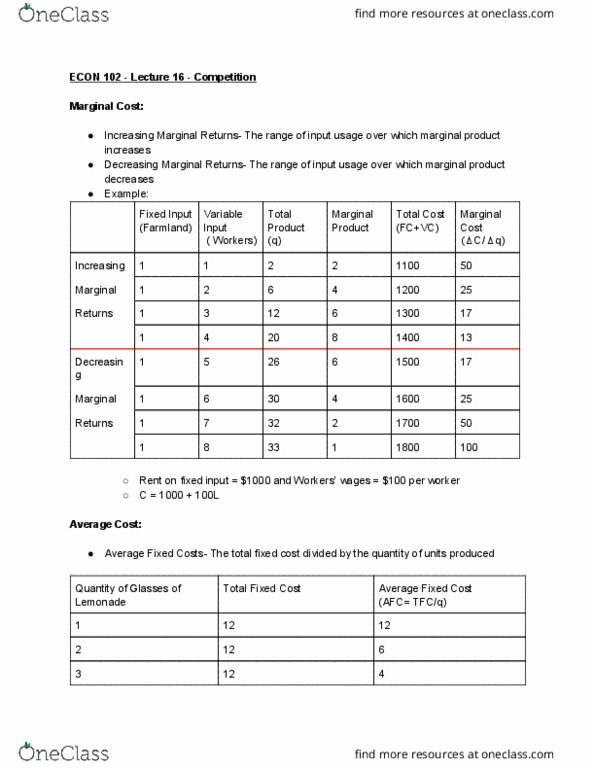

Price: the amount of money the buyer has to spend to buy it from the seller. Cost: the amount of money the seller has to spend to produce it. Total cost: the cost of producing a certain quantity of units of a good. Fixed costs: costs that do not vary with the quantity of units produced. Variable costs: costs that vary with the quantity of units produced. Marginal cost: the cost of producing one more unit of a good. Law of diminishing marginal returns: with a fixed input, and an increasing variable input, at some point the marginal product of the variable input must decline. Marginal product: the additional output produced when one more unit of variable input is added. Increasing marginal returns: the range of input usage over which marginal product increases. Diminishing marginal returns: the range of input usage over which marginal product decrease. Average fixed costs: the total fixed cost divided by the quantity of units produced.