MGT 181 Lecture Notes - Lecture 6: Expected Return, Systematic Risk, Market Risk

25 Dec 2015

School

Department

Course

Professor

Document Summary

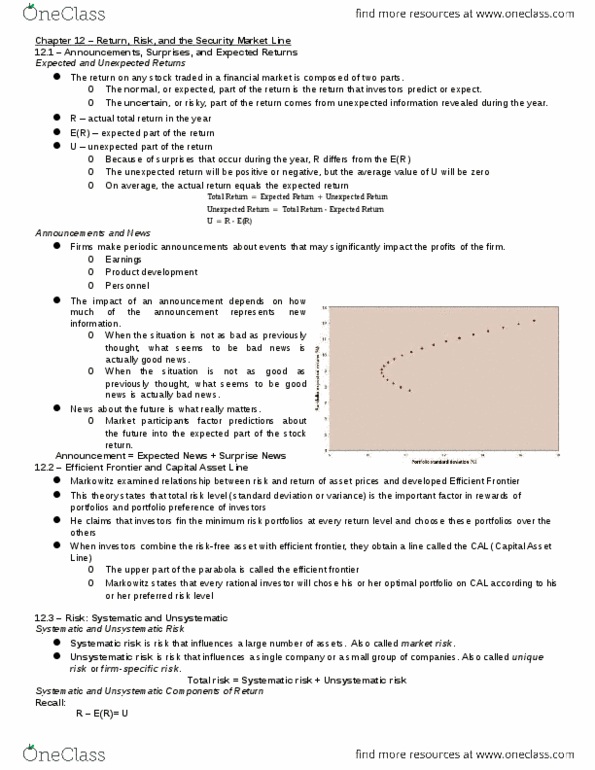

Expected returns are based on the probabilities of possible outcomes. An asset"s risk and return are important in how they affect the risk and return of the portfolio. The risk-return trade-off for a portfolio is measured by the portfolio expected return and standard deviation, just as with individual assets. The expected return of a portfolio is the weighted average of the expected returns of the respective assets in the portfolio. Expected vs unexpected returns: realized returns are generally not equal to expected returns. At any point in time the unexpected return can be positive or negative. Over time, the average of the unexpected component is zero. Announcement and news contain both unexpected and expected components. Efficient markets: they are a result of investors trading on the unexpected portion of announcements. The easier it is to trade on surprises, the more efficient markets should be. Efficient markets involve random price changes because we cannot predict surprises.