ACCT 2001 Lecture Notes - Lecture 4: Tax Rate, Tax Avoidance, Filing Status

67

ACCT 2001 Full Course Notes

Verified Note

67 documents

Document Summary

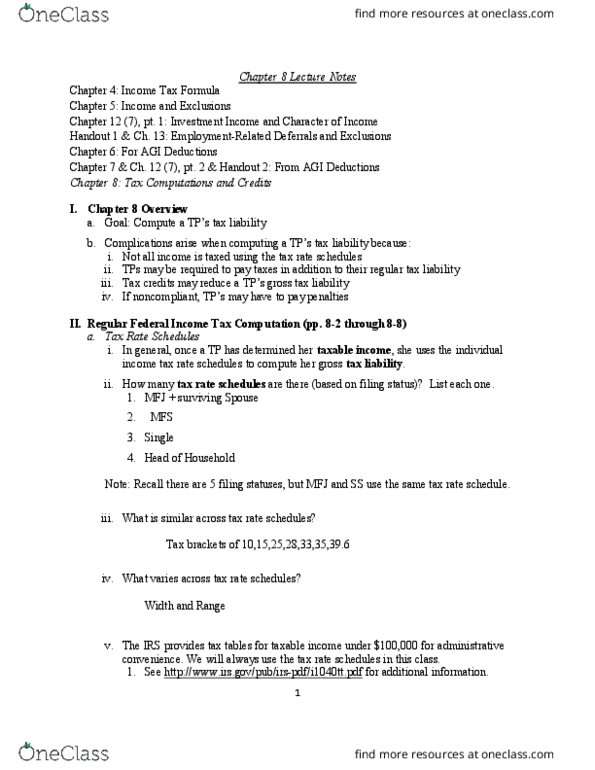

Chapter 8: tax computations and credits: overview deductions for agi, deductions directly related to business (pp. 6-2 through 6-23, deductions indirectly related to business (pp. 6-23 through 6-33, deductions subsidizing specific activities (pp. 6-33 through 6-37) Deductions directly related to business (pp. 6-2 through 6-23: as a matter of equity, because congress taxes income generated by business activities, Any loss not currently deductible is carried forward indefinitely. By definition, capital assets generally do not include business assets: what schedule are these expenses reported on, loss limitation rules. 2: in general, business expenses reduce net income and are fully deductible. How do these categories interact: passive activity income or loss , portfolio income , active business income . Ned is the 100% owner of a rental property in winterfell. Ignoring the rental property, ned has other income of 80,000. The rental property generates ,000 of rental income each month, but ,000 of expenses. Example 1: allocation of rental expenses between personal and rental days.