FINA 365 Lecture 5: Week 5 2.7.17

8 Feb 2017

Department

Course

Professor

Document Summary

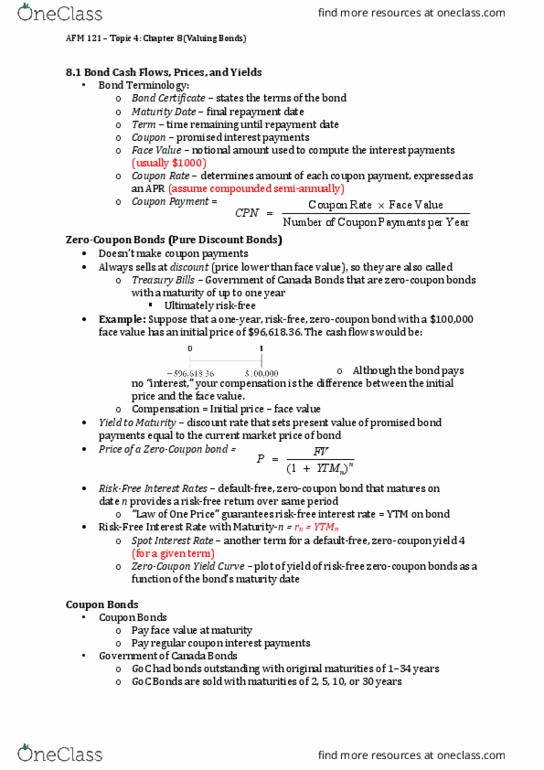

Purchase a 30-year, zero-coupon bond with a ytm of 5%. For a face value of 100, the bond will trade for: Bond"s ytm stays at 5%, the price will be higher 5 years later. Rate of return : (29. 53/23. 14)^. 2 -1 = 0. 05. As bond moves closer to maturity, price approaches face value. Effect of time on bond prices is predictable, but unpredictable changes in rates also affect prices. Bonds with different characteristics will respond differently to changes in interest rates. Investors view long term bonds to be riskier than short term bonds. More time for things to happen that will impact the value of the bond. Long term bonds are more sensitive to interest rates than short term. Consider a 10 year coupon bond and a 30 year coupon bond with 10% annual coupons. By what percent will the price of each bond change if its ytm increase from 5 to 6.