FIN 350 Lecture Notes - Lecture 6: Interest Rate Risk, Put Option, Call Option

37 views3 pages

Document Summary

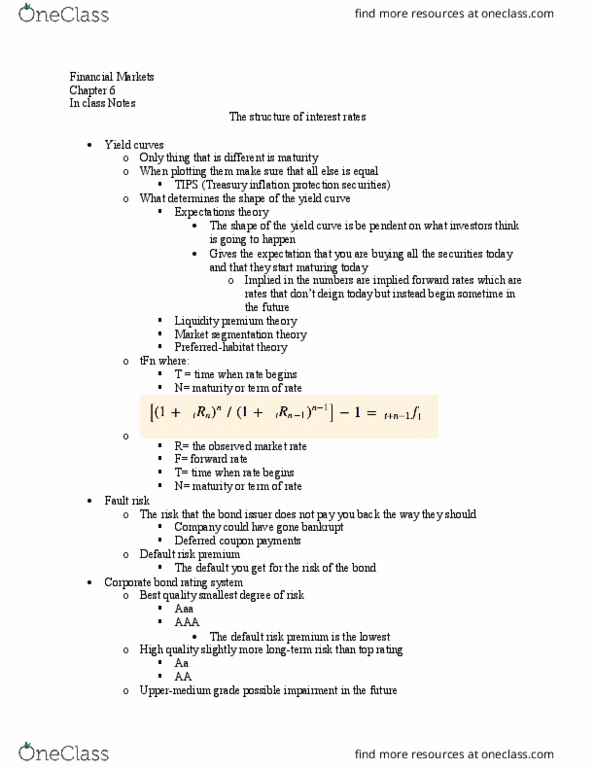

All have a par value of 1,000: the amount of money borrowed. All have a coupon rate: the interest being paid on this loan, usually paid semi annually. All have a maturity: the point in time in which the bond gets paid, you can have a one year, mid-year 3-5, long term 10yr or. The contract of the bond spells out the par value, coupon rate, maturity and any special things: options. Call option- when a person can sell the bond at a certain time with a specific price in the indenture. Put option- the option of the company to force and buy it back from you has a set price in the indenture: sinking funds. The price of a bond can be represented as: cf/ (1+i)^1 + cf/(1+i)^2 . Yield to maturity: the one interest rate the will discount the cash flows back to the price of the bond.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers

Related Documents

Related Questions

You plan to buy a car 3 years from now and plan to take out a 3-year car loan. Given the following yield curve and assume that the spot rates are continuous compounded, what will be the interest rate for your car loan?

| Yrs to Maturity | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| % yield | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

2. Given the following treasury bonds, calculate the 18-month zero rate. Assume face value of each bond is 100 and coupons are paid semi-annually.

| Bond | Yrs to Maturity | Annual coupon rate% | Bond price |

| A | 0.5 | 0 | 98 |

| B | 1 | 8 | 98 |

| C | 1.5 | 9 | 104 |