ACCT 23021 Lecture Notes - Lecture 11: Comprehensive Planning, Strategic Planning, Regional Policy Of The European Union

2 Aug 2020

School

Department

Course

Professor

Document Summary

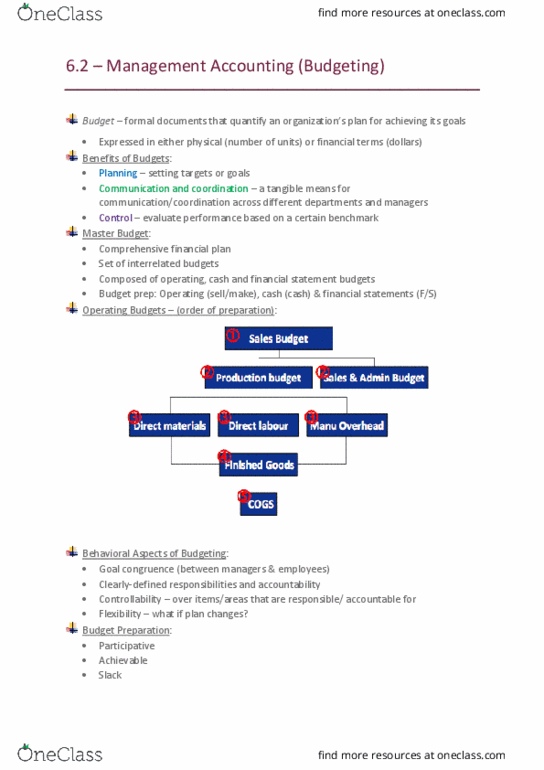

9. 1 describe how and why managers use budgets. Begins with company"s overall mission or purpose statement. Strategic planning: setting long-term goals that extend 5 to 10 years into the future. Rolling budget: continuously updated so that the next 12 months of operations are always budgeted. Participative budgeting: involves participation of many levels of management. More likely to be motivated by a budget they helped create. Use prior year budget or actual results as the starting point. Zero-based budgeting: managers begin with a zero budget and must justify every dollar. Operating budgets: needed to run daily operations of the company; culminate in budgeted income statement. Financial budgets: include capital expenditure budget and cash budgets; culminate in budgeted balance sheet. Example: tucson tortilla expects to sell 30,000 cases at a price of per case. 30,000 cases x per case = ,000. Decide how many units the company needs to produce.