ACC 442 Lecture Notes - Lecture 6: Engagement Letter, Preliminary Ruling, Audit Risk

describe the standard on communications between predecessor and successor auditor.

Successor is required by auditing standards to communicate with the predecessor auditor. Due to

confidentiality the client must consent to this communication and the purpose is to determine if the

client lacks integrity or if there were disputes about accounting principles.

What kind of inquires should be made to the predecessor?

Did you have any disputes about accounting principles? What types of problems did you have

communicating with the client?

Describe purpose of engagement letter

Provides the engagements objective so the client knows exactly what they are agreeing to.

Describe contents of engagement letter

details of the services the auditor is going to perform, when they will be performed, and the cost of

performing them.

Define related party

...

what is the related parties importance to the auditor

...

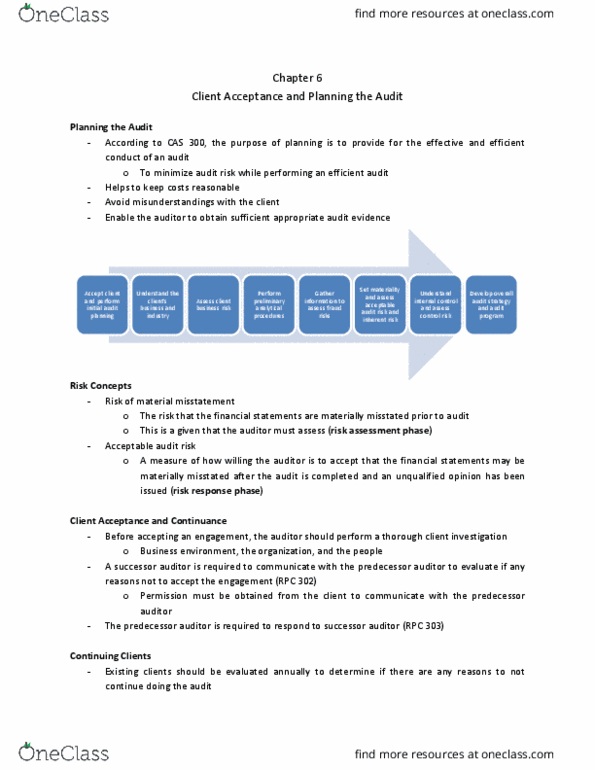

Describe how an auditor obtains knowledge of the clients industry and business

Determine risks of specific industry, familiarity with industry risks, familiarity with accounting reqs of

certain industries.

Auditor identifies major sources of revenue, key customers, tours clients facilities, and identifies related

parties.

Define materiality

the magnitude of misstatements that individually or when aggregated with other misstatements could

reasonable influence decision of users i.e. (Is something relevent enough to influence the decision of the

statement users)

find more resources at oneclass.com

find more resources at oneclass.com

describe the process of obtaining preliminary judgement about materiality

using professional judgement to create a judgement about materiality that can be changed throughout.

It is a judgement by an auditor that is the most an audit could be mistated by and still not affect

materiality of the audit.

Discuss the relationship of materiality to audit evidence-not as important

...

what qualitive factors affect materiality-not as important

...

what are the different types of risk assessment procedures?

Inquires of management and others

Analytical procedures

Observation and Inspection

Discussion among team members

Other risk assessment procedures

Role of risk assessment

Provide input for understanding entity-Help auditor id and assess risk-Used to develop audit strategy

plan in response to assessed risks.

Describe the audit risk model***

PDRIRCR=AAR.

Figure 9-2

Figure 9-3

Define inherit risk

suceptability of an assertion to material misstatement

define control risk

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Describe the standard on communications between predecessor and successor auditor. Successor is required by auditing standards to communicate with the predecessor auditor. Due to confidentiality the client must consent to this communication and the purpose is to determine if the client lacks integrity or if there were disputes about accounting principles. Provides the engagements objective so the client knows exactly what they are agreeing to. Describe contents of engagement letter details of the services the auditor is going to perform, when they will be performed, and the cost of performing them. Define related party what is the related parties importance to the auditor. Describe how an auditor obtains knowledge of the clients industry and business. Determine risks of specific industry, familiarity with industry risks, familiarity with accounting reqs of certain industries. Auditor identifies major sources of revenue, key customers, tours clients facilities, and identifies related parties.